By EastGate Shipping Inc

Dry bulk freight earnings surged to multi year highs in 2021 thus far and summer season did not put breaks on the accelerated rebound with Capesize earnings surpassing the US$50,000/d mark. The rosy sentiment of the second quarter came against the traditional summer lull and market values continued their upward trend. Buyers’ appetite appeared strong for all bulker ship sizes, as smaller ships, Handysize and Supramax, maintained a consistent and stable increase in freight earnings.

Secondhand investments

The first eight months to August have shown the total number of bulker sale and purchase transactions exceeding 700 vessels, compared to about 300 deals concluded at the same period last year. The current picture drives the activity to be one of the highest in the last decade with the Baltic Exchange Secondhand Assessments signaling an enormous rally of upward trend.

For a 5-year-old vessel, Capesize values have increased to US$43.9m beginning of September, marking a 39% y/y increase. In the Kamsarmax segment, the level of increase is even higher at 42.4% with prices around US$30.3m. The highest y/y increase has been registered in the Supramax segment, nearly 68%, where we also see stronger appetite from buyers with values at US$25.6m and Handysize vessels follow. The 5-year-old Handysize values are now sitting at region US$22.6m, up by 53.5% y/y.

This upcycle in asset values confirms that the supply/demand fundamentals look very promising for the future prospects of dry bulk earnings. That being said, the Chinese economy showed signs of slowdown during August as the Caixin China General Manufacturing PMI fell to 49.2 in August 2021 from 50.3 in July, missing market estimates of 50.2.

This was the first contraction in factory activity since April 2020, dragged down by containment measures to curb rising cases of the Delta strain, supply bottlenecks and high pricing of raw materials. However, the sentiment remains buoyant with expectations that the recovery of freight earnings will be sustained for a significant period of time as the global economy and seaborne trade are both recovering from the major pandemic challenges.

Overall, August brought a lot of activity in the Handysize segment for vessels built 2012-2016 and 2007-2011. In the Capesize and Panamax segments, there was some activity but not at the same firm levels of Handysize secondhand purchases. Supramax bulkers continue to attract investors’ interest at the same age preferences with Handysizes.

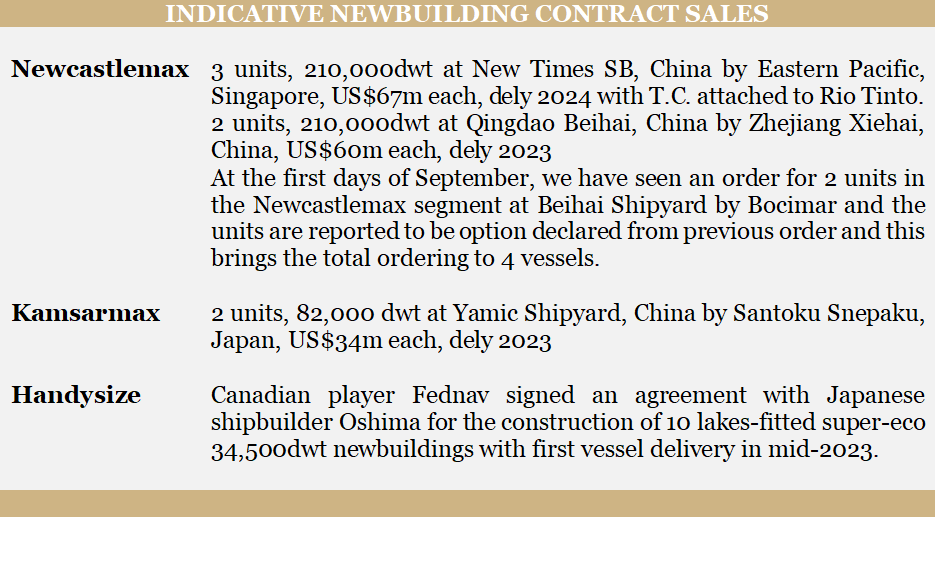

Newbuilding market

Summer season brought firm volume of new orders. Chinese shipyards attracted the lion share of new activity with presence mainly in the Newcastlemax, Kamsarmax and Ultramax/Supramax segments. The total volume of new orders, however, remains at a low territory: during the first eight months of 2021, total contracting activity stands a tick over 100 orders, about half of the contracting activity conducted in 2019.

In the meantime, newbuilding prices have also peaked to levels not seen for at least a decade, while the record freight earnings is likely to stimulate further appetite for new orders. Newbuilding prices for a Capesize vessel are now standing at about US$60m, which is 28% above the values at the beginning of the year. In the Kamsarmax segment, the increase is higher to about 38%, with prices around US$36m and in the Ultramax, even higher with 43% increase at prices around US$33m.

Overall, there was a flow of new orders in August mainly by Asian players. Firm activity in newbuilding contracting meant an incoming volume of new units added to the orderbook, while Kamsarmaxes attracted the most interest. Five new orders came to light for Newcastlemax bulkers, 8 in the Kamsarmax, 4 in the Panamax, 2 in the Ultramax, 2 in the Supramax and 6 in the Handy segment.

Fleet update

For the first eight months of this year, scrapping activity has been rather thin with vessels heading to the scrapyards not exceeding 65 bulkers.

Dry bulk deliveries this year have added 26.7m of deadweight and the existing fleet has increased YTD to 934m dwt, according to latest estimates by BIMCO. Further, the world’s dry bulk fleet is projected to grow to 940m dwt by year-end which, if realised, would mean a 3% y/y increase.

The current picture of the dry bulk orderbook stands at around 54m deadweight, down 44% from 2019 levels and allows some positive signals for the persistent increasing trend of freight rates. The current percentage of orderbook to the existing fleet is circa 7% and of course the question remains as to how much of the capacity will be demolished in the coming months. The high earnings environment admittedly discourages further scrapping with projections suggesting that this year’s scrapping volume will not exceed 7m dwt, less than half of what was removed from the market in 2020

Conclusion

In conclusion, the overall fleet-to-orderbook picture provides a promising outlook for freight earnings and elevated price assessments, both for secondhand and newbuilding tonnage, going forward. There are expectations that the rebound of the Chinese economy will trigger demand growth which is possibly going to absorb most of the available tonnage supply. Fleet utilisation projections are also very positive and although last year’s figures remain sub 85%, far below the high utilisation achieved in 2008 (~98%), they are suggestive of new record levels to be achieved (~90) by 2022 as orderbook capacity is standing at historical lows.

In our infographic below, you can view the evolution of secondhand bulkers’ values this year: