By Jeffrey Landsberg

In recent weeks, more provinces in China have been announcing that they will be reducing steel production as the central government continues to voice that it wants to cap 2021’s crude steel production at 2020’s total. While it is virtually impossible that China’s crude steel production this year will total no more than 2020’s year’s record 1.05 billion ton total, steel production will certainly continue to come under some government-mandated pressure. However, we remain of our view that steel production this year will ultimately not come close to contracting. As we also have examined in our Weekly Dry Bulk Reports and Weekly China Reports, we must continue to stress that China’s iron ore imports historically are not simply based on the performance of crude steel production.

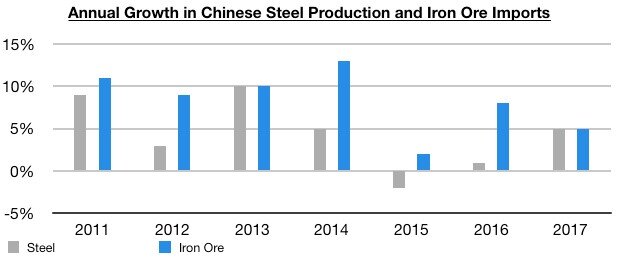

Examining the last ten years of crude steel production and iron ore imports shows that China’s iron ore imports have stayed resilient during each year where China’s crude steel production growth came under notable pressure. Last decade began with China’s crude steel production growing year-on-year by 9% in 2011, and iron ore imports that year grew year-on-year by a robust 11%. However, 2012 then saw China’s crude steel production grow year-on-year by only 3%, but iron ore imports that year still grew year-on-year by 9%. 2013 saw strong growth in both crude steel production and iron ore imports (each grew by 10%), but then 2014 saw crude steel production grow year-on-year by 5%. However, iron ore imports in 2014 still grew year-on-year by 13%. 2015 then saw China’s crude steel production contract year-on-year by 2%, but iron ore imports that year still grew year-on-year by 2%. 2016 then saw crude steel production grow year-on-year by only 1%, but iron ore imports that year grew year-on-year by 8%. 2017 saw the same growth in both crude steel production and iron ore imports (each grew year-on-year by 5%).

As we have been stressing in our work since we started our consultancy in 2010, it is global iron ore production that dictates China’s iron ore import volume. China has long remained content to purchase as much iron ore that exporters want to sell China (as imports are much higher quality than iron ore mined in China). Year after year has continued to show that China’s actual iron ore import demand remains resilient even when crude steel production growth comes under pressure.

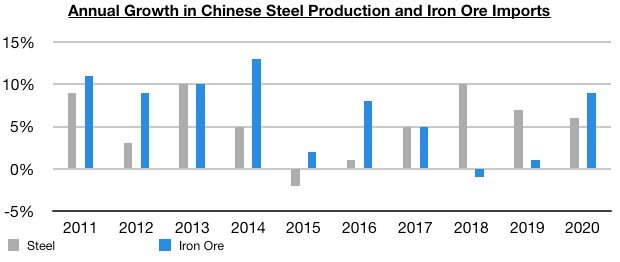

2018 and 2019 would then go on to see weakness in iron ore imports, but this was not due to weakness in crude steel production. China’s iron ore imports contracted year-on-year by 2% in 2018 and grew year-on-year by only 1% in 2019, but crude steel production grew year-on-year by 10% in 2018 and by 7% in 2019. It was not weakness in steel production that led to two years of iron ore import weakness. Global iron ore production was not finding significant growth at this time following years of weakness in iron ore prices, and overall global iron ore production was also hit further in 2019 after Vale’s dam collapse in January 2019 (which ended up curtailing Vale’s production). 2020 then ended up seeing China’s crude steel production grow year-on-year by 6% and iron ore imports grow year-on-year by 9%.

As we have often discussed in our work, it is actions in China that are much more telling to us than any government statements (or lack of statements). Overall, year after year has continued to show that China’s actual iron ore import demand remains resilient even if steel production growth comes under pressure. During the last ten years, there have been three years where China’s crude steel production grew by less than 5% (2012, 2015, and 2016) — and during all of these years China’s annual iron ore imports set new records (iron ore imports during these years also grew year-on-year by an average of 6%, while crude steel production during these years averaged growth of just 1%). The central government never comes out and states that iron ore imports can easily continue to grow even during years where steel production growth comes under pressure, but this is exactly what history has continued to show. While restrictions on China’s steel production are not supportive, China’s iron ore imports are likely to continue to find strength this year as long as iron ore exporters continue to ramp up their production. Consuming as much imported iron ore as possible (at the expense of domestically mined iron ore) remains in the very best interest of China's environment.