By Ulf Bergman

The International Monetary Fund (IMF) has in recent days reiterated its global growth projection of six per cent for the year. However, maintaining the headline number masked the fact that some nations, notably wealthy ones, had their projections upgraded, while many developing nations are expected to see lower growth rates, due to vaccine shortages and resurgent infection rates. India saw its forecast growth slashed by three percentage points to 9.5 per cent, due to the damage done by the recent serious coronavirus outbreak and a continued shortage of available doses of vaccine.

As the second wave of infections is starting to recede, the economic activity is expected to see a revival. The Indian steelmaker JSW Steel Ltd. has recently said that it expects domestic steel demand to increase by seventeen per cent to 110 million tonnes in the year that began in April, which would be a new record. According to the company, the rising power consumption and mining activity, along with higher vehicles sales is pushing up demand for the metal. Construction is also expected to pick up in the coming month, adding to the bullish outlook for the sector.

Despite the severity of the recent coronavirus outbreak, Indian seaborne imports of coal have held up remarkably well in the last two months. Both months recorded healthy year-on-year gains and are only marginally below the levels seen in 2019.

An economic recovery living up to the expectations of the IMF is likely to see coal imports remaining strong, both for thermal and coking coal. The projected pick up in economic activity and industrial production is likely to fuel an increase in demand for electric power, which could drive the volumes of imported thermal coal higher during the second half of the year. The projected increase in steel production will also drive the Indian demand for coal higher, both for the coking coal used in the production process and the thermal coal as the increase in production will drive the electricity requirements higher.

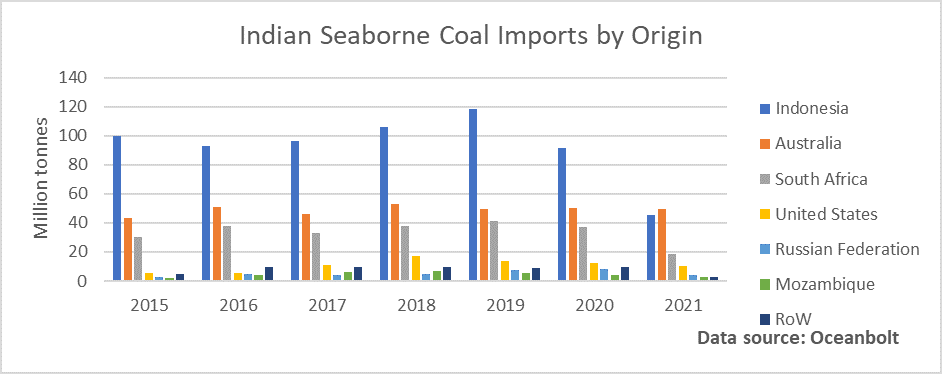

The ongoing diplomatic fracas between China and Australia shows no signs of improving, with Australian coal exports being one of the largest victims. Since the unofficial import ban came into effect during the second half of last year, a very limited number of vessels carrying Australian coal have been allowed to dock in China and discharge their cargoes. So far this year, no vessels have left Australian ports with coal destined for China. The embargo saw Australian coal miners losing their main customer virtually overnight, the Chinese move was as sudden as it was unexpected. Based on the volumes from 2019, Australian producers needed to find alternative markets for 85 million tonnes of coal as a result.

The Indian market has so far proved to be a good alternative market for Australian miners, with large parts of the coal volumes normally destined for China now shipped there instead. In the first seven months of the year, Australia has shipped 50 million tonnes of coal to Indian ports. The volumes are equivalent to what has been dispatched during a whole in the past. Indonesia on the other hand has lost its previously dominant position in the Indian market, with export volumes to India looking set to fall well below the 118 million tonnes shipped in 2019. Indonesian coal is now increasingly shipped to China, as a replacement for the banned Australian coal.

The ongoing diplomatic spat between China and Australia has not only altered the trade flows of coal, but also the deployment of vessel types. Previously, the Panamaxes were the most common tonnage for bringing coal to India, but in the last year, the crown has shifted to the Capesizes. Likewise, China’s increasing reliance on Indonesia for its seaborne coal imports have shifted the focus to Panamaxes in that trade.