By Ulf Bergman

There is no shortage of headline-grabbing events at the moment, with many of the items having the potential of derailing the global economic recovery. The rapid change in sentiment has been quite a turn-around from the optimism of previous months when the pandemic and its effects were perceived to be in retreat. The energy crisis is by no means the only dark cloud on an otherwise blue sky.

Extensive bipartisan political wrangling in the US has led to the federal debt approaching its legal limit, which would result in a default on federal payments and a shutdown of many governmental functions. While the US Senate has reached a deal that allows the debt ceiling to be raised and staves off a US default on federal payments, the respite is merely temporary. New problems may arise as early as December when the new agreement reaches a new upper threshold.

The Chinese economy faces its own fair share of problems. The difficulties in the property sector, highlighted by the Evergrande debacle, has paled into insignificance next to the squeeze on energy supplies but are nevertheless still very relevant and hurting sentiment. Manufacturing slipping into contraction territory in the latest PMI survey has also added to the woes. Any hopes that the Golden Week would provide a welcome boost to consumer sentiment appears to be premature, with early indications suggesting road travel is down by a third compared to pre-pandemic levels and two per cent lower than last year. However, the recent reports that the Chinese leadership has ordered major utilities to secure coal and natural gas for the winter season "at any cost" highlights its ambition not to let the economic growth slow too much. The move is also somewhat at odds with previous environmental initiatives but suggests that additional stimulus programmes may be on the cards.

Beyond the domestic problems in the world's two largest economies, the continued disruptions to the global supply chains are also putting downward pressure on economic growth globally. A shortage of components and materials has affected industrial production worldwide, with output shrinking in some cases. On top of this, there are rising geopolitical tensions, with much of it focusing on the South China Sea.

The immediate effects of the energy crisis are blackouts and electricity rationing, negatively impacting production and economic growth. However, a longer-term problem is the rising production costs that will fuel inflation. While coal and natural gas have given up some of their recent gains following a Russian announcement that it intends to export more gas to Europe, prices remain close to their highs and are likely to contribute to rising inflation rates. The combined effects of rising inflation and economic growth coming under pressure have led some economists to suggest that the world faces a period of 1970s-style stagflation.

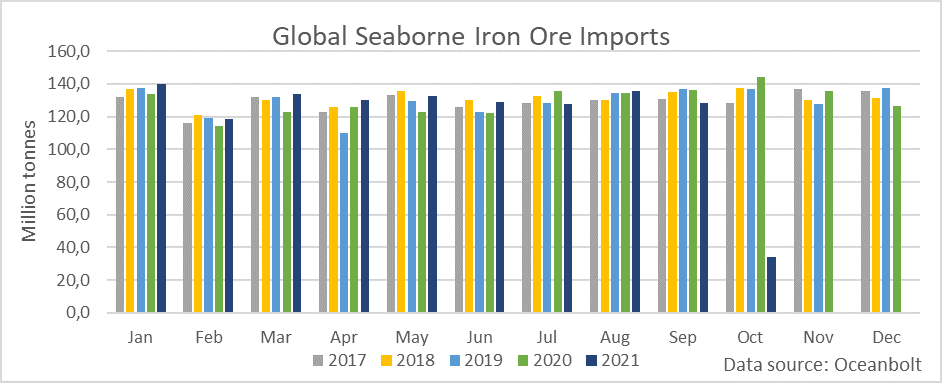

The more problematic outlook for the global economy saw global seaborne volumes of the major dry bulk commodities coming under pressure in September. After a strong reading in August, iron ore imports fell back in September to the lowest levels since 2016, according to data from Oceanbolt. The reduction was, to a great extent, the result of the Chinese clampdown on steel production. However, the final quarter has begun strongly, with the first week of October implying a monthly volume in line with the same month last year.

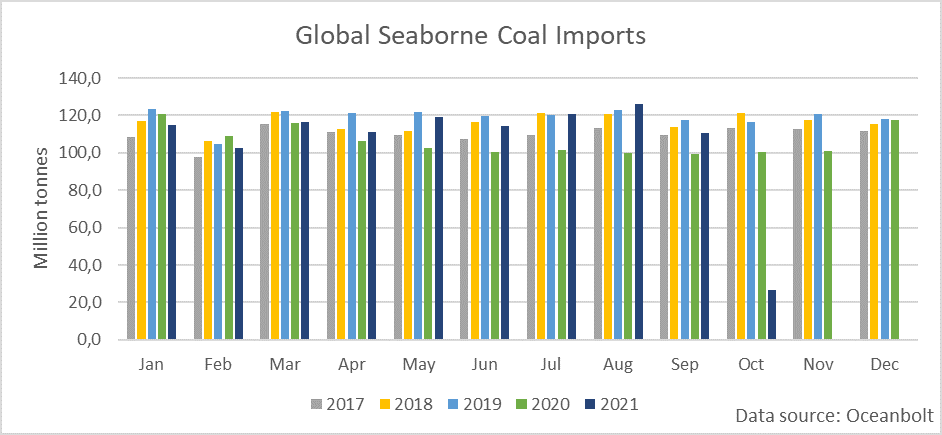

For coal, the picture is similar, with volumes falling during September compared to the previous month. Unlike for iron ore, last month's seaborne quantities were larger than a year ago. Assuming a degree of linearity, volumes in the early part of October suggest that around 120 million tonnes of coal will be discharged in ports during the month. This would be at par with the highs of previous years. However, the global rush to restock coal inventories could see August's record volumes challenged in the coming months.

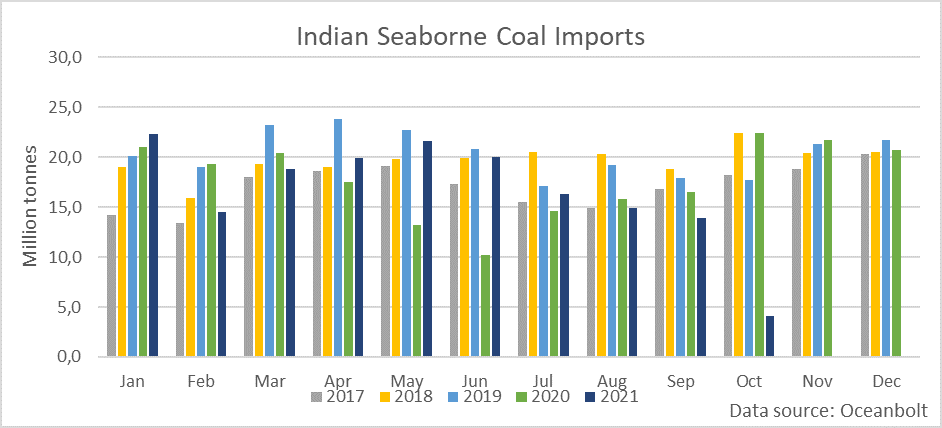

India could contribute to record seaborne coal volumes, as the country's coal inventories are critically low. Although the problem has been known for some time, the quantities of imported thermal coal have declined in recent months. The trend appears to have reversed, with October volumes already matching 30 per cent of the previous month. Given the low stockpiles in India, there are concerns that extensive powercuts could damage the prospects for what is widely expected to be one of the best performing economies this year.

The energy crunch is likely to remain in place for some time, possibly for the duration of the winter in the Northern Hemisphere. The low inventories in the two largest importers, China and India, will force both to keep their imports elevated to avoid excessive damage to their economies. Continued strong demand for thermal coal would benefit tonnage demand, especially if additional natural gas exports could force prices south. At the same time, slowing growth brought about by rising energy costs could dampen the enthusiasm for commodities and seaborne transportation. However, Beijing's recent strong statement of intent suggests that all tools will be used to avoid an economic slowdown. Hence, despite fears of a soft patch for the global economy, the appetite for commodities is unlikely to soften too much.