It was exactly a year ago, when we published a piece on the impending correction of Capesize rates that at the time were hovering around decade-highs of ~$35,000, a number that today might sound amusing to most market observers dealing with spot rates that are rapidly approaching $100,000. Then, over the next few months, rates corrected some 70% reaching almost $10,000 by mid-December, once again demonstrating the cyclicality of the industry but also the extreme volatility that characterizes the spot rate market.

Fast forward to today, and Capesize spot rates are sitting at ~$90,000, with prognosticators calling for a breach of the symbolic $100,000 mark soon, a very substantial move in the historically “sleepy” dry bulk market (which was the case for at least the past decade). At the same time, bulk commodities are also experiencing some of the most extreme moves in history, with coal prices hitting new all-time highs daily and iron ore prices having already visited the $200/ton range for the first time ever (although it is important to note the sizable drop in the last several months to now “only” $120/ton).

In this environment, dry bulk shipping once again has demonstrated the extreme leverage it possesses when it comes to the commodity cycle. From the large Capesize ships to the “yawning” Handymaxes, returns have exploded to levels unimaginable just a year ago. With such drastic moves, the future becomes even more uncertain, as macroeconomic drivers, especially as it relates to China, are rapidly shifting, leaving investors and market participants at a crossroads when it comes to the near-term direction of spot rates, especially in the highly volatile Capesize segment.

It has been all one big trade: European coal prices and Capesize spot rates

Our view remains that we are at or close to an inflection point and although spot Capesize rates always might have more room to rally, the risk of focusing on such incremental gains (especially given the diminishing nature of percentage gains) outweighs any return potential.

We expect that by December spot rates would have been halved, and although futures are already at a significant discount to spot, it is unlikely that the market will recognize such value until the spot index bottoms. Which of course is also the good news: the forward curve has so far failed to rally to the same degree that spot Capesize rates have, opening the potential for incremental gains down the road on a highly backwardated 2022 curve (more on the mechanics of that later).

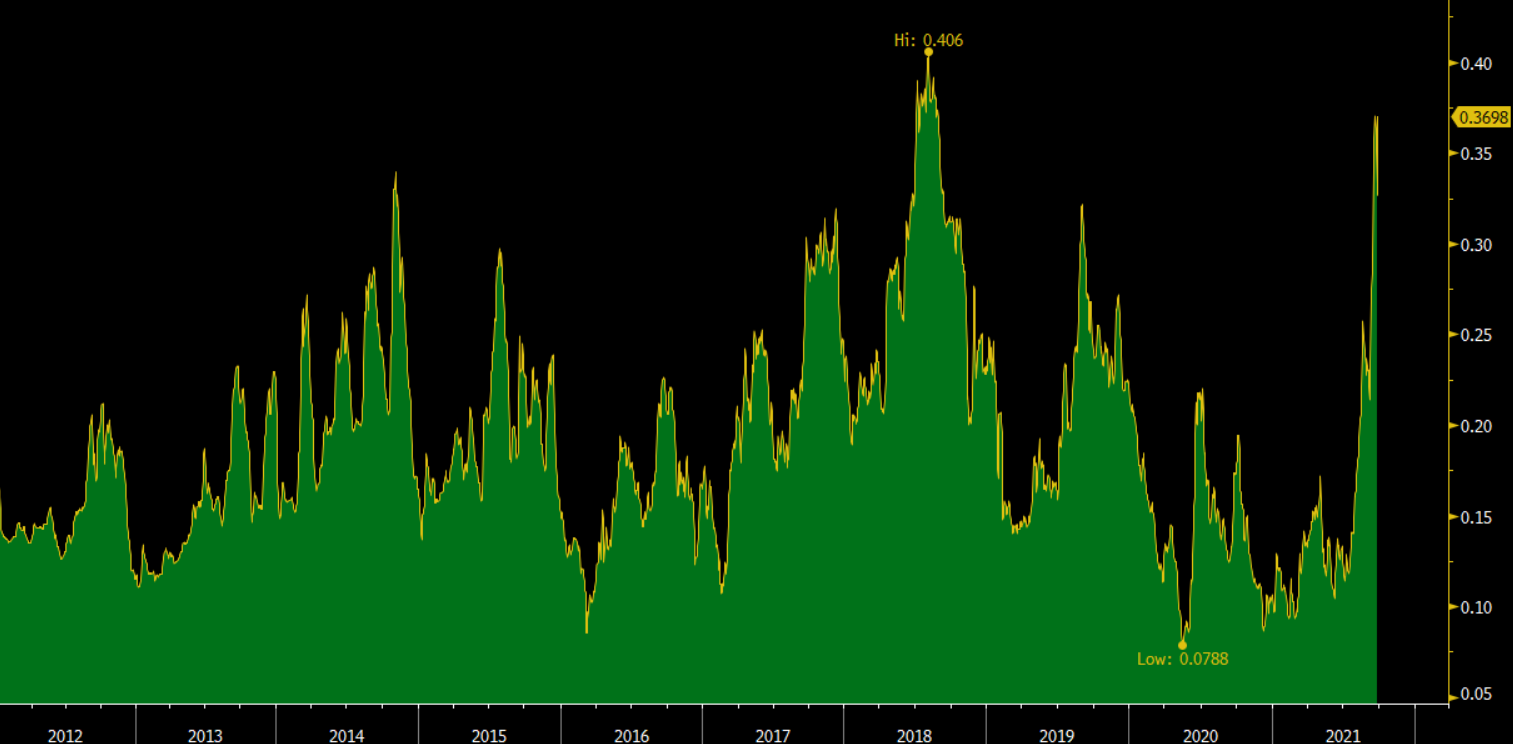

Then, there are the economics of trading: Freight transportation costs should not be taken in isolation to the underlying commodity price that’s being transported. Although each market has its own demand and supply fundamentals, over time, there is a link between freight and commodities, particularly when prices reach extreme levels in either direction. At such an environment, FOB and CIF prices begin to make a huge difference for traders as the risk of freight rate volatility becomes a real issue.

Freight as a percentage of iron ore delivered price (62% IO and Brazil-China freight, Capesize)

The main reason for our cautious stance has to do with demand. Although we are very aware of the considerable bottlenecks around the world when it comes to shipping, demand rules, and any softening could lead to a major loss of confidence on the part of owners. In containers, such a drop might already be underway, with a sharp decline in freight costs in a very short period of time. For dry bulk, a similar scenario is not unthinkable, although the way the spot market operates, especially for Capesizes, makes it a less likely event.

Yet, as we look at the economic activity in China, where 2/3 of dry bulk demand originates, we cannot construct a near-term bullish story for dry bulk. Yes, energy is in short supply globally, and coal-derived energy will play a key role this winter, but the reason that coal prices are at record highs is also due to the limited supply of the material and as a result shipping volumes will also potentially be capped. Iron ore, which is the main commodity transported by Capesize vessels, has so far failed to provide any significant growth on the demand side (we think global production growth this year will be marginal). Throw on top the significant curtailment in steel activity driven by the Chinese government, and it is tough to get too excited about the near term outlook.

Which leads us to the supply, the key parameter across shipping today. Congestion remains an issue, and there is very little visibility on how that develops. But as one can easily understand, it is not the overall supply of the global fleet that is lagging behind demand (at least not yet). It is the bottlenecks across the supply chain that are causing freight prices to spike. There are enough ships around, just not in the right spots. Yet, we have watched the numbers around port congestion fluctuating violently over the last year, and thus we have less confidence on the sustainability of such bottlenecks, especially given that not only it originates, but it also hurts, the ultimate consumer for most commodities, namely China.

In our near term forecast, as spot rates “return back to earth”, the cycle is by no means over. Rather, it is a natural progression of shipping, and as we have always been stressing out, it is averages that matter. The fourth quarter will end up being the strongest quarter of the year, an argument we have been making for the past six months now against market consensus, as seasonality once again has returned to the Capesize market.

Furthermore, as expected, spot rates will be much weaker in the first quarter of next year, but substantially above previous years, subject to relatively normal for the season weather in the southern hemisphere.

How much of the above is priced in the futures market? A lot. Actually, one can argue more than it should be, but again, the dry bulk market has historically experienced some brutal corrections and thus we see no reason to be heroes at this point in time with Capesize rates at 2008 levels.

Capesize 2-month futures minus spot at extremes…

{kind=link}

The backwardation in futures (meaning futures prices are lower than spot and the further out you go, the cheaper it becomes) is an opportunity, but not necessarily just because of relative pricing. As explained above, there is a valid reason why the first quarter of the year is currently priced at a ~70% discount to the spot market.

Our advice is to remain humble but also to be ready to take advantage of overreactions in a potential looming correction in the spot market, as futures traders will remain skeptical until the spot bottoms, something that we believe could happen at higher than expected levels and thus provide the opportunity to enter into positions that will proven to be profitable.

What if we are wrong? Well, this is also a likely scenario, as the driver of current strength remains vessel availability due to supply chain constraints. However, we remain confident that any continuation of the current trend will be measured in days. Unfortunately, drivers around such days-long modeling are impossible to obtain, and the risk of being wrong, at least very near term, is high.

Icarus flew too close to the sun, and as a result his wings melted and fell apart. Capesize rates are flying high at the moment, but fundamentals are not necessarily there (yet) to sustain such a high altitude. What does mythology teach us?