By Ulf Bergman

The global competition for the limited supplies of thermal coal continues, and, with no sign of any immediate relief, prices keep pushing higher. While early trading on Thursday saw coal futures retreating on the Chinese commodity exchange in Zhengzhou by almost five per cent, the January contracts eventually ended the session some three per cent above Wednesday’s close. The most actively traded contract has now gained approximately 25 per cent in the last three sessions, as traders continue to bet that supply shortages will remain the narrative. The escalating electricity shortfall in many provinces highlights the challenge authorities face to deliver power to homes and heavy industries. While domestic production has been increasing, the recent flooding in the Shanxi province, China’s most significant coal-producing region, adds to the woes.

Official Chinese data show that coal imports surged by 76 per cent in September, compared to the same month in the previous year. While not quite record-breaking, the 32.9 million tonnes imported by land and sea rank among the highest volumes ever recorded. However, some of China’s leading suppliers have struggled to maintain the flow of coal, with land-based imports from Russia and Mongolia restricted by limited rail capacity at the same time as adverse weather conditions have hampered Indonesian exports.

Elsewhere, the US is on track to increase its use of coal in power generation, according to the Energy Information Agency (EIA). Despite an ambition by the Biden administration to phase out the use of the black stuff and eliminate carbon emissions from the power grid, coal will supply 24 per cent of the electricity this year, after falling to a historical low of twenty per cent in 2020. In Europe, the promise of additional supplies of Russian natural gas has seen prices retreating from recent record highs. However, prices remain very high from a historical perspective and could still force many utilities to opt for the relatively cheaper coal.

In light of the push by many countries and utilities to secure supplies for the winter, seaborne export volumes have recovered to broadly the pre-pandemic levels of 2019 in recent months. With the mid-point of October rapidly approaching, some approximately 52 million tonnes of coal have shipped globally and put the month on track for narrowly falling short of the 2019 readings. Allowing for a degree of delay in additional coal shipments to materialise, the seaborne volumes in the coming three months may exceed the pre-pandemic average levels of 120 million as countries scramble for extra supplies.

After a dip in seaborne imports during September as port congestion and production problems in Indonesia took their tolls, increasing volumes of coal has been discharged in Chinese ports. According to data from Oceanbolt, some 12 million tonnes have been imported so far in October, which would suggest that the total for the month could surpass 27 million tonnes.

Since July, Europe, often seen as one of the leading forces in the decarbonisation process, has seen its coal imports returning to pre-pandemic levels. The continent’s domestic LNG production lags behind demand. At the same time, supplies from top seller Russia have been limited, driving the European buyers to the global market and contributing to the surging natural gas prices. The tight supply situation for natural gas and record-high prices has seen demand for the dirtier fossil fuel back in vogue. While Russia remains the dominant player in the European coal market, the Australian market share has increased as the diplomatic ruckus with China is forcing it to find alternative customers and adding a healthy amount of tonne-mile demand to the trade. US exports of coal to Europe has also increased, with volumes in October likely to be the highest since January 2019.

Many of the more significant coal exporters recorded Q3 exports above the levels seen in 2019, with only Australia, Colombia and South Africa substantially below pre-pandemic levels. Hence, rapidly increasing supplies significantly could be a challenge. However, the latest annual report from the EIA suggests that spare capacity is available in the US coal mines. Additionally, South African exports are recovering after several months of disruptions due to the pandemic, civil unrest, and train derailment. The export volumes during October could be the highest since March.

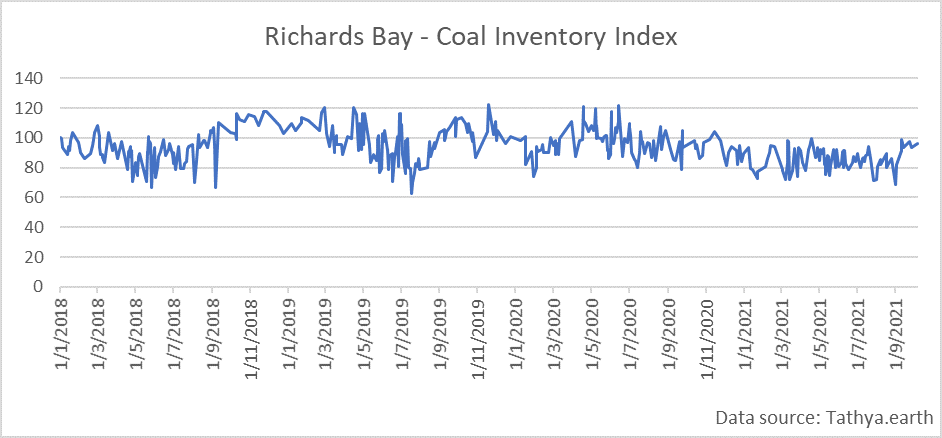

The outlook for the South African exports looks promising, as coal inventories are recovering in the port of Richards Bay. According to satellite data from Tathya.earth, the downward trend for the stockpiles in the port has been broken during the latter part of the third quarter. In recent weeks, inventory levels have returned to what was last seen in April.

Elevated coal prices look set to be the theme for the coming winter in the Northern Hemisphere. Many years of limited investments in new coal production capacity have resulted in the tight supply situation, with only a handful of producers still capable of ramping up output. For the largest importer, China, as long as the ban on Australian coal remains in place, any additional volumes are likely to be found in more distant locations such as South Africa, Colombia and the US, which will add to the tonne-mile demand.