By Nick Ristic

Despite accounting for a quarter of the dry bulk fleet, Handysizes rarely make the headlines. But relative to the larger ships, the segment has performed extremely well over the past couple of years. We look at the supply and demand drivers behind this trend.

A flying start

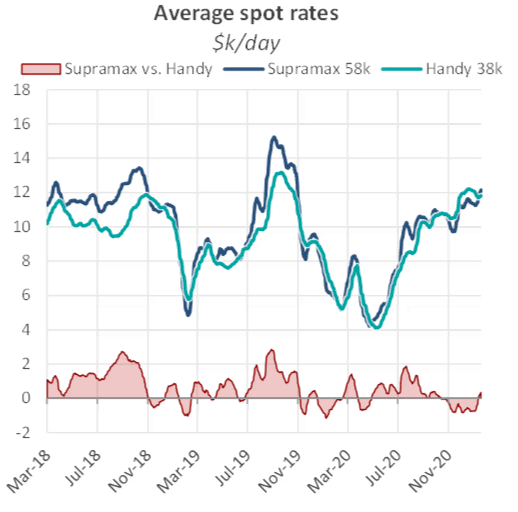

As we covered last week, the dry market has started 2021 on good footing, as a rarely-seen January rally extends into the second half of the month. And the Handy market has been no exception. The Baltic Exchange’s 38k dwt Handysize index has averaged over $11,835/day so far this year, 63% higher versus the same period in 2020. Based on the 28k dwt index, which has been published for longer, current rates are 70% higher than average January levels over the last five years.

However, while the Supramaxes are also performing well, the premium that they typically earn over Handies has continued to erode, a trend we have seen emerge over the past couple of years. The Supra-Handy spread swings in the short-run, due to fluctuating strength in regional markets, but in 2020, Supramaxes earned on average just $185/day over the 38k dwt Handies, down from $656/day in 2019 and $1,162/day in 2018.

One can debate whether these indices are accurate measures of the rates that owners of these ships actually receive, but we see the same trend occurring in the period market. Based on our one-year timecharter assessments for ships of the same specifications, Supramax returns averaged only $713/day more than the Handies in 2020. This is down from $975/day in 2019 and $1,815 /day in 2018.

Undersupplied?

A clue as to why this differential has narrowed may lie in the supply-side of the fundamentals picture. The Handy market appears to have been spared the excessive supply growth that has plagued the larger vessels. Since the start of the big delivery years in 2008, the Handysize fleet has grown by a modest 29%. Over the same period, Supramax capacity has swelled by 164%, while the Panamax and Cape fleets have grown by 106% and 136% respectively (see p.15 for fleet definitions).

Looking only at recent history, 2020 saw hefty fleet additions in the dry market, but again Handy deliveries have been vastly outpaced by those of the bigger ships. Last year we recorded 138 new ships come onto the water within our broader Supramax Category boosting the size of this fleet in dwt terms by 3.6%. Within this, the relatively new Ultramax fleet grew by 13.6%. Meanwhile, Handysize additions in 2020 only pushed this fleet’s carrying capacity up by 1.6%.

This mismatch could in part explain why average Handy rates have been closing in on those in the Supramax market, which are being weighed on by a flood of new Ultramax tonnage. The pattern looks set to continue. At just 4% of current fleet capacity, the Handysize orderbook is the lowest of any dry bulk sector, 2 percentage points lower relative to Supramaxes.

Breaking down demand

The demand-side of the equation also likely plays a role in this relationship. By aggregating all Handysize and Supramax trade flows, including ballast voyages, we can measure the relative importance of different commodities to demand for each shipping sector. The most stark difference between the Handies and Supras in this demand breakdown is on coal. The Supramax market is heavily exposed to this good, which accounted for around a quarter of demand over 2019-20. The Handysizes meanwhile only depended on coal for about 10% of their demand over this period. Instead, Handies appear to be much more focused on the grains, which accounted for 26% of demand over the last two years, versus 19% for the Supramaxes.

Given how these different commodities have been impacted by the pandemic, it is unsurprising that demand for Handies has been somewhat more robust than for Supramaxes over the last few months. Global coal trade slumped by almost 10% YoY in 2020, as we saw a sharp drop in both power demand and steel production outside of China. Being more dependent on this commodity, the Supramax markets took a relatively greater hit to demand. In addition, for most of 2020 China imposed strict import controls on thermal coal imports while it tried to boost domestic production. This disproportionately hit imports from Indonesia, a key demand region for Supras.

The grain trades meanwhile continued to grow in 2020 as food demand remained resilient and many producers enjoyed favourable weather conditions. Total grain volumes increased by 5% YoY, and while this boost was enjoyed by all of the geared ships, it likely supported Handysize rates to a greater extent as grain accounts for a larger share of demand in this market.

Handies are also more exposed to the fertiliser trades which fared well last year. The various fertiliser products account for 11% of Handy demand compared to 7% for Supramaxes and a boost in long-haul shipments from the Baltic and European continent to countries in the Americas and Southeast Asia helped to buoy Handy rates in 2020. At the same time, Supramaxes tend to be more heavily focused on the minor ore trades, especially nickel ore, which saw volumes plunge at the start of 2020 following an export ban from Indonesia. Nickel ore trade accounted for almost 5% of Supramax demand in 2019 and less than 1% for the Handies, so a 30% reduction in shipments last year put a greater dent in demand for the larger vessels.

Looking forward, ordering patterns and the contrasting growth prospects for both grain and coal trade seem to support a continuation of this trend. However with the commodity landscape extremely volatile, as we progress through the year we will likely see varying trade growth stories continue to affect the Handy-Supra relationship in different ways. Just over the past few weeks, as China has relaxed controls on thermal coal imports, we’ve seen a surge in Supramax trade that has again pushed up rates relative to Handies.

And as global investment and raw material demand recovers, the key takeaway is that we remain positive on the long-term prospects for both the Handy and Supramax markets, which are well placed to take advantage of a rebound in minor bulk trade.