As the new month begins, it was a positive day for dry bulk rates with futures moving higher and now standing well above 20,000/day for Capesizes for the next several months. The upcoming seasonal increase in dry bulk demand is ahead of us, but another unexpected factor might exaggerate any potential increase in freight rates, causing more confusion in an already turbulent year.

According to broker reports, in the last several days, China has increased COVID-19 screening for crew members, which means longer delays in discharging ports and thus higher congestion.

In fact, some agents are today reporting that the Lianyungang/LYG Municipal Government is requesting all vessels who had called/visited foreign ports within 14 days (no matter had crew change or not) to quarantine at anchorage without exception.

Such delays are also causing concern among buyers as they increase freight costs, especially for grain buyers.

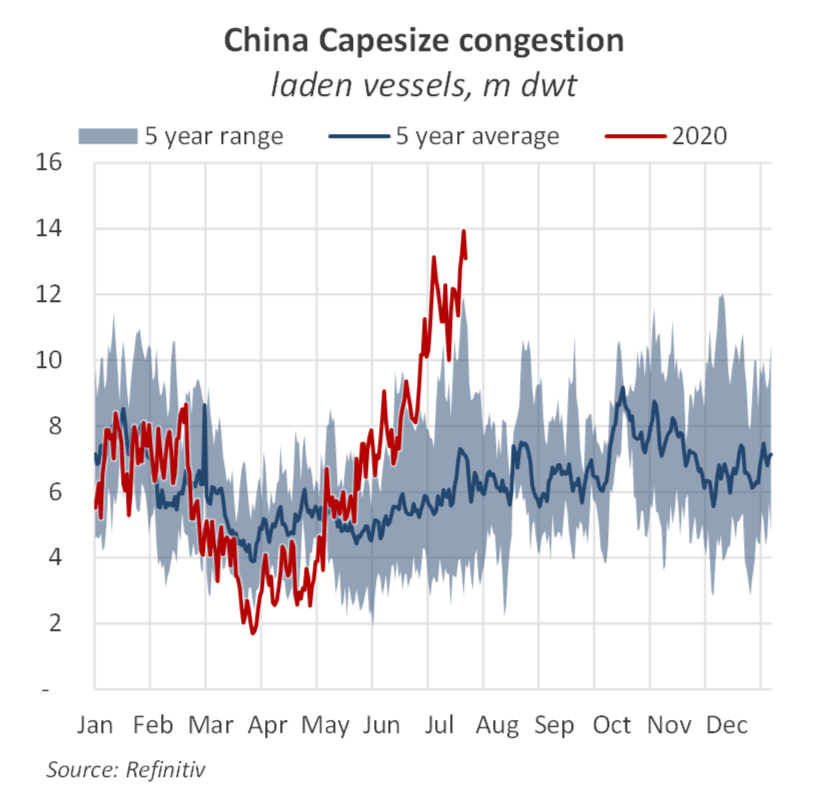

With congestion remaining at record highs, such a development will further tighten the market, leading to potentially higher rates in the near term, as ballasters take longer to reach the Atlantic while the Pacific will also see reduced tonnage in the near term. Will such a development cause another spike in spot rates similar to June?