By Ulf Bergman

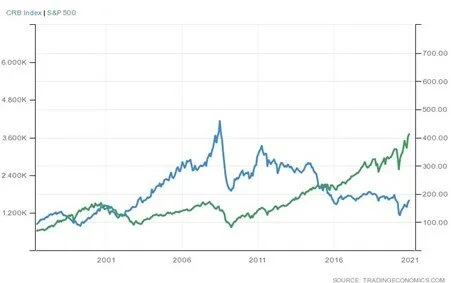

As cyclical assets come, commodities are to be found somewhere around the top of the list. Typically, the asset prices and investor interest fluctuate with the fortunes of the global economy. The first decade of the millennium saw commodity prices soaring as the Chinese economy became more and more integral to the global supply chains. The beginning of the financial crisis some twelve years ago, put an end to the boom years and the asset class have been pretty much out of favor with mainstream investors ever since. On a composite level, commodities have struggled during the last decade, as many parts of the world failed to regain much of the traction lost during the recession following the problems in the banking sector. At the same time the equity markets have flourished, with artificially low interest rated and various quantitative easing programmes pumping liquidity in the financial markets.

Thomson Reuters/Core Commodity CRB Index vs. S&P 500

The post-COVID-19 economic recovery in China has driven prices for many commodities, such as iron ore and copper, sharply higher from their lows during the second quarter. Prompting Chinese authorities to put pressure on producers and a domestic derivatives exchange to bring the rising prices under control. Iron ore futures have been especially popular among some investors as a proxy for directional bets on the Chinese recovery, which has contributed to prices heading north in combination with several issues that have tightened the physical supply.

Despite the recent strong run for a lot of commodities, many investors and analysts argue that it is only the beginning of a lengthy bull market for commodities. Among others, the investment bank Goldman Sachs believes we are entering a commodities super-cycle that could compete with the gains seen during the oil boom in the 1970’s or the China-driven increases in the beginning of the 2000’s.

A resurgent global economy, fueled by extensive fiscal and monetary stimulus, would, as vaccines are rolled out, add to China’s already strong demand for commodities and support a bullish outlook for commodities. This could potentially derail China’s recent attempts to temper the rising prices, but also give the producers a strong incentive to maximize their output and, hence, serve to dampen the impact of rising demand on prices. Brazil’s iron ore output has suffered in the wake of the dam collapse and heavy rains and is producing less than it did a few years ago. The current high prices are likely to hasten a recovery in Brazilian output volumes, with a stabilizing effect of prices and adding to the demand for dry bulk tonnage.

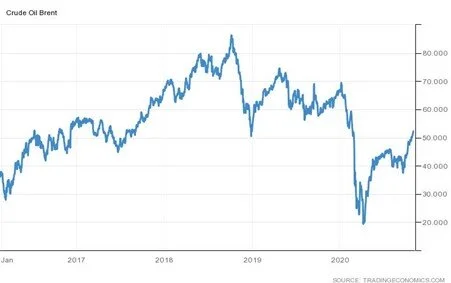

Beyond iron ore, copper is one of the pundits’ darlings, with prices expected to rise further, as the demand for electrical wiring increases with a recovering industrial production. Like for iron ore, there are some concerns of a growing disconnect between the physical and the futures markets, with a risk for a price correction unless the physical market catches up. The roll out of vaccines is also likely to lead to a recovery in the market for crude oil, as positive vaccine news already having led to price gains. An increasing need for transportation and energy, combined with the production cuts implemented by OPEC+, will see higher oil prices. However, the recovery may prove somewhat short-lived, as the cartel relaxes the production cuts and the energy transition gathers pace.

Brent Crude Oil (USD/barrel)

It is not only the narrative of a post-pandemic recovery in demand for commodities that makes the asset class attractive for many investors. The size of the fiscal and monetary measure that are being put in place to help the economies to recover will see a dramatic rise in government debt levels and we can expect to see inflation rates to increase. As commodities are a natural hedge against inflation, it can be expected that the asset class will see an additional inflow of money. Over the last five years around 130 billion dollars of passive investments have flowed out of commodities, but rising inflation rates could see some, or all, of that returning to the asset class and pushing up the prices. An inflow of money from institutional and retail investors is likely to be channeled towards the paper rather than the physical market, with the derivatives market continuing to have a significant impact on commodity prices.