In the following weeks Klaveness Research will in a series of articles have a look at how we believe the fundamentals impacting dry bulk freight rates are shaping up for 2021.

In the first article we started off by having a look at the big picture. In the second and third article, we drilled further down into the details of the seaborne iron ore and coal market. This week’s article will be on the seaborne grains trade. In subsequent reports we will drill further down into the other commodity groups of minor bulks and bauxite before we finish off with a look at the supply side.

The link between the grain trade and dry bulk freight rates

We include all grains, oilseeds and sugar in the commodity group named Grains. The commodity group of grains had a 12%* market share in total dry bulk trade measured by volume 2019 (left chart below). The demand for vessels cannot simply be derived from volume - we need to take distance and trade inefficiencies into account as well - as time spent on the total transport work is what ultimately impacts the aggregated demand for vessels. Also, for some cargoes like grains, it is the area of the hulls which is the restricting factor and not the carrying capacity in terms of tonnes. As an example, let’s say we use a Kamsarmax with a dwt of 82,000 on voyage from Santos to Yantai with soybeans. Due to the high stowage factor of soybeans the vessel would only be able to load about 71,350 tonnes. However, if the cargo instead had been iron ore then the intake would be about 80,500. Thus, everything else equal you would need 13% more vessel capacity measured in dwt if the cargo is soybeans than if the cargo is iron ore. If we measure grains share in total dry bulk trade by using the Dwt x Duration metric we end up with grains having a market share of 17% in 2019 (chart in the middle below), which is substantially higher than the volume based market share of 12%. In the first ten months of 2020 the market share of grains has increased another percentage point.

If we break it down by segment, we see that 41% of all seaborne grain volumes were carried on Panamaxes in 2019 (right graph below), followed by Supramax and Handysize at 29% and 26% respectively and lastly short sea vessels at 4%. The Capesize market share is virtually zero. If we pivot and instead look at the market share of grains in each vessel segment’s carrying capacity, the geared Supramax and Handysize segments grains has a market share of 20% and 24% respectively (middle graph). This is substantial but far less than the market share of minor bulks. In the Panamax segment grains was the second most important commodity in 2019 with 38% of vessel demand, slightly behind coals market share of 42%. The grain market share in Panamax demand has increased to 42% in the first 10 months of 2020 while the market share of coal has fallen to 39%.

For all the segments we see that grain has a higher market share when we use the Dwt * Duration calculation than if we look at volumes, but this tendency is clearly most pronounced in the Panamax segment. The reason is that while all segments have the effect of the high stowage factor for grains, it is the Panamax segment which is the preferred carrier of long-haul grain shipments such as soybeans. As grains is a substantial part of the demand for all segments except Capesize the link between the grain trade and dry bulk freight rates in these segments is direct and clear. But the grains market is also important for the Capesize market in periods of high utilization and earnings. Due to economies of scale the Capesize segment can normally offer the cheapest freight on a per ton basis. When Cape utilization is high it leads to higher freight rates which from time to time makes Panamax freight less expensive on a per ton basis. When this happens, we often see cape splits, which is negative for the Capesize market as it results in cargo volume flowing from the Capesize segment into the Panamax segment. When long-haul grain volumes are in high season it increases the utilization in the Panamax segment, which increase Panamax freight and thus raises the threshold of where Cape splits are triggered.

Grain supply and demand

The United States Department of Agriculture (USDA) is an undisputed authority when it comes to Agricultural projections. USDA expects the global grain trade to increase marginally in the 20/21 marketing year (+1.2%) from a high base in the 19/20 marketing year (MY). If USDA’s estimate for the current marketing year is correct, then the average growth rate in the previous decade will end up at an impressive 4.9%. In terms of volume, coarse grains (corn, barley, sorghum, oats and rye) makes up the largest sub-group of grains, followed by wheat, major oilseeds and major protein meals. The coarse grains group has seen the strongest growth rates in the last decade with a compound average growth rate (CAGR) of 6.7% followed by oilseeds at 5.9% while wheat and protein meals has seen weaker growth at 3.6% and 1.6%. The average sailing distance of oilseeds, in particular soybeans, is by far the longest. Thus, in terms of vessel demand the largest growth driver in the last 10 years has been the oilseeds. This has been a very positive demand driver for the Panamaxes which is the preferred carrier of long-haul grains.

By far, the three biggest export regions of grains are East Coast South America (ECSA), North/Central America and the Black Sea (Med/BS). These three export regions collectively represented 87% of total grain export volumes in the 2019/2020 marketing year. Other noteworthy export regions are the EU and Australia. Med/BS has recorded the highest percentage growth rates in the last decade (+13.5%) followed by ECSA (+6.0%). In absolute volume terms the growth has been by far highest from ECSA. North America recorded negative growth rates in export between 17/18 and 19/20 due to the trade war with China. This has lowered the average growth rate in the last decade to 2.7%. The grain exports out of Australia, the EU and the rest of the world (ROW) has hardly recorded any growth in the last decade.

In the current marketing year USDA estimates that North American export will rebound sharply (+19%) as China is back buying grains from the US. ECSA has increased their market share in global grain export substantially in the previous two years when US export has been curtailed by the trade war. This trend is broken this year with export expected to decrease 7.5%. Exports out of the Med/BS is also predicted to decrease with 7.5% due to higher competition from the US. Australian export is predicted to make a big comeback in the 20/21 MY after very weak export in the previous two years as a result of draught. Australian grain export – primarily – is predicted to increase from 15.5Mt in the previous two years to 25.8Mt, an increase of 66%.

While the Pacific only accounts for 22% of grain exports, 58% of the import are in the Pacific. On the demand side, 58% of the imports is in the Pacific, with Far East and South East Asia as the largest demand centers. While on the export side, only 22% is in the Pacific. As the major grain export regions are in the Atlantic it means that the average distance of the grain trade is very long. If we look at export vs import per basin only on Panamaxes (the preferred carrier of long-haul grains) we see that 80% of imports are in the Pacific, while 84% of the export is in the Atlantic. If we look at the geared segments imports are higher in the Atlantic than in the Pacific, suggesting that the trade is more intra-basin than in the Panamax segment.

2020 grain trade figures – A very strong year

Global grain trade is up 6.3% in the first 10 months of the 2020 calendar year, based on trade flow data. Monthly export volumes have been at seasonal all-time high levels for every month except of January.

ECSA grain export was exceptionally strong in the Q2 peak season and is up 4.5% year to date (ytd) October. However, exports were down year on year (yoy) in September and October due to strong competition from the USA. Nevertheless, grain export out of ECSA has had a very strong run since May 2019 and is likely to stabilize at a high level in the 2021 calendar year. USDA expects total grain export to be down 12 million tonnes (Mt) in the coming 20/21 marketing year - which counterintuitively starts in Q1-21. Brazilian planting has been running late due to draught and it is thus widely expected that the harvest will be later than in an average year. This, suggests that export in Q1 will be fairly weak compared to recent years.

US grain exports were weak in the previous two years because of the trade war with China. This year’s peak export season has started of at all time high levels as China is buying massive amounts of soybeans and corn from the US.

Ytd grain export out of the US is up 15% while exports in the last two months alone are up 71% yoy. Exports in October was a new monthly all time high. Outstanding sales of grains and oilseed are currently at unprecedented levels. Outstanding sales means cargo sold but not yet shipped. Combined outstanding sales of soybeans, corn, wheat and sorghum is at 67 million tonnes as of 05th November, this is comfortably a new all-time high – up 42% from the previous all time high in 2013 and up 177% yoy. The record outstanding sales strongly suggests that the export pace of will continue at a very high pace in the coming months. Coupled with the fact that the Brazilian harvest is running late it is very likely with continued high export in Q1.

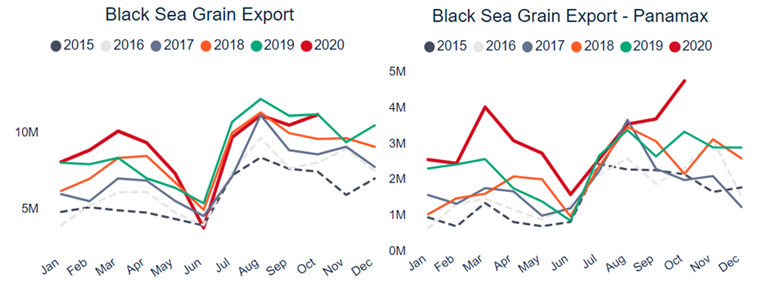

Exports out of Med/BS – the third largest grain export region – is up 1.9% in the first 10 months of this year. Total grain export was recording seasonal all-time highs in the first 10 months of the year but has been down yoy since June. However, if look at Panamax shipments there is no signs of weakness in recent months. Panamax grain exports out of the Med/BS has been very strong as long-haul shipments of corn and barley to China has been on the rise.

Have you heard about the Chinese pig herd?

One of the biggest demand drivers for Panamaxes is the soybean trade from ECSA and USA to China. Chinese soybean imports were growing at a strong linear pace between 2011 and 2017. The average yearly growth rate within this period was a stellar 10.4%. However, that trend was abruptly broken in 2018, partly due to the trade war between US and China but primarily due to the devastating effect on Chinese feed demand from the African Swine Flu. Most of the grain import is not used for human consumption but as a feed ingredient for breeding livestock and poultry. One of the largest demand centers for feed grains in China is the pig herd. Culling of pig herds became widespread as the Chinese tried to stop the virus from spreading. When the size of the Chinese pig herd bottomed out in October 2019 the size of the herd was down 40% YoY. Since then the size of the herd has been growing and growth rate has accelerated after the summer. We now see soybean imports increasing fast again. Imports in the last 12 months is up 35% from the preceding 12 months period. We do expect the growth rates in Chinese soybean imports to slow down compared to what we have seen in the last 12 months, but we will not be surprised if we get closer to the average growth rates between 2011 and 2017 at around 10%.

We expect the Chinese import of other feed ingredients such as corn to grow at a strong level in the coming years. China has for many years been building up their domestic reserves of grains. The Chinese stocks of corn climbed from 43Mt in 2010 to 223 Mt in 2017. However, in recent years there has been a deficit of corn in China resulting in declining inventories. USDA did a big revision in their forecast for Chinese corn imports in their latest monthly report, up from 7 to a record 13Mt. However, we still thing USDA is running behind in their upward revisions of Chinese corn imports as total commitments from US alone is at 10.7Mt. In addition, we have at least 1.1Mt on the water from other countries. With the current marketing year lasting until September next year we are confident that we will see more positive revisions from USDA in the coming months.

As mentioned above, USDA expects the global grain trade to increase marginally in the 20/21 marketing year (+1.2%) from a high base in the 19/20 marketing year. We think there is considerable upside from that estimate, primarily due to rapidly increasing Chinese corn demand. Our estimate would be a YoY growth in the 2021 calendar year of at least 2% for the global grain trade. As we believe that the long-haul Chinese corn imports has the biggest upside, we expect vessel demand to exceed the volume growth.

Grain demand – How is the long-term outlook?

Once a year USDA publishes their long-term projections for the coming 10-year period. In their latest long-term publication from February they project strong global income and urbanization growth in the coming decade. Increasing per capita income and population growth are among the major factors driving increasing global trade in agricultural commodities and products. World economic growth is projected at 2.7% from 2020/21 through 2029/30. The economies projected to grow the fastest are in Asia. Per capita GDP in South Asia and Southeast Asia will rise at average annual rates of 5.0% and 3.8%, respectively. The world’s population was 7.5 billion in 2019. A projected annual growth rate of 0.9% means that roughly 703 million people will be added to the world’s population over the next decade. Many developing countries are not well-suited for increasing production of specific commodities. In those countries, consumption may increase faster than domestic production, leading to growing imports of agricultural commodities and products. Growing global demand for agricultural commodities, especially by low-income countries and emerging markets, leads to increasing world imports over the projection period. USDA expects the trade to grow for all the projected agricultural commodities. The U.S. trade disputes with China that existed at the time when the projections were formulated dampened expectations, particularly for soybeans. The projections assumed the trade disputes to continue for the duration of the projection period. Thus, there is considerable upside in these projections as China today is back and buying U.S. beans and corn in a big fashion.

To summarize we expect global grain trade in the coming calendar year to grow with at least 2% in volume terms, and more in terms of vessel demand. The long term outlook for trade growth is positive as the global population continues to increase and as a rising middle class in Emerging Asia switches to a more protein rich diet. The lions share of demand growth will be in Asia while the export will continue to grow the most in the Atlantic. This means that growth in vessel demand will be healthy, especially in the Panamax segment which is the preferred carrier of long-haul grains.

Next week we will take a closer look at how the fundamental drivers for minor bulks is shaping up for 2021. In subsequent reports we will take a closer look at the bauxite trade before we finish up the series with a look on the supply side.

*All trade growth numbers in this article is derived from our in-house analytical platform which includes data and material from AXSMarine, all rights reserved.

** We use the following segmentation rules: Capesize (100kdwt+), Panamax (70-100kdwt), Supramax (40-70kdwt), Handysize (10-40kdwt), Other (<10kdwt)