By Nick Ristic

Covid and dry bulk

While the pandemic has had a catastrophic effect on most markets, dry bulk demand seems to have fared relatively well. In March, we saw supply chain disruption and port closures, but those have since dissipated, and in terms of prices, many of the key dry bulk commodities have outperformed other goods. This is in part down to supply disruptions (particularly in the case of iron ore) but is also due to sustained demand for raw materials and ‘essential’ goods, such as grains.

As we covered last week, economic growth forecasts have been upgraded, which has filtered into our demand outlook, though prospects vary greatly across the major commodity groups.

The steel complex and iron ore

China’s steel market has outperformed our expectations this year. The economy has recovered swiftly since Q1, following apparent containment of the pandemic, and a round of stimulus spending earlier in the year has helped to buoy construction and manufacturing activity. We also saw speculative interest in China’s the steel market increase steel producers’ margins, as investors bet on a V-shape recovery through the commodity markets. Crude steel output in China over the first nine months of the year totalled 783.3m tonnes, a 4.7% YoY increase. In the short term, we expect to see output cool, as weaker construction activity and winter pollution controls come into force. Chinese iron ore demand however should not fall to the same extent, as restocking continues into the final weeks of the year. Looking to the longer term, we still see China’s steel demand slowing, and electric arc furnaces playing a greater role in the production mix. Just this week we heard that that the next five-year economic plan in China will mandate greater use of scrap steel and stricter pollution controls. We see these factors driving a plateau in Chinese iron ore imports, though the strength in steel output this year has raised the baseline from which demand will soften.

Elsewhere in the world, steel industries are still suffering hefty losses in output, but we have upgraded our forecast for their recovery to growth. The hit to global steel output this year was sharp, but not as long-lasting as that following the global financial crisis. 2020’s recession has turned out to be far different to that a decade ago, in that the services industry, rather than manufacturing and construction, has been hit the hardest. Our forecasts for iron ore demand across the other major steelmaking regions reflect these changes.

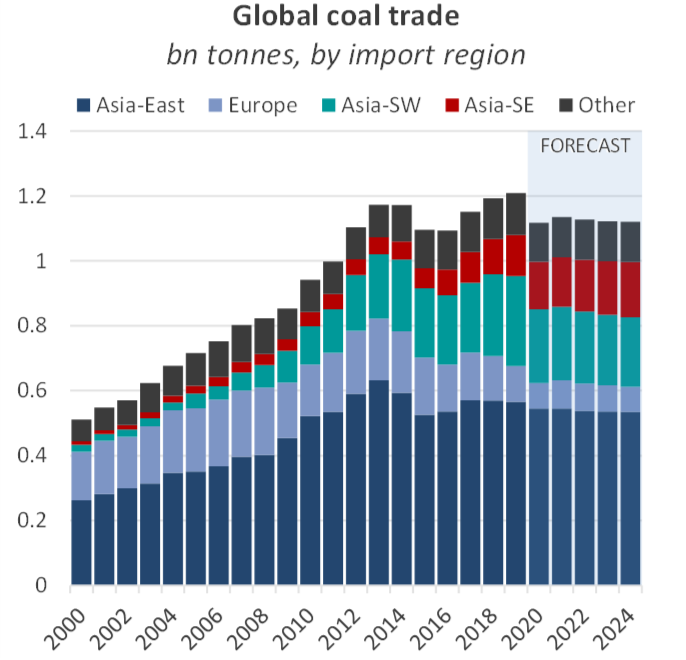

Coal outlook revised

In the dry bulk world, coal has been the commodity that has seen the greatest level of demand destruction this year, and we have had to revise down our forecasts of demand from the coal trades going forward.

The main drivers of the Asian coal market, China and India, have seen significantly weaker coal imports over the past few months. India, following severe lockdowns, saw sharp contractions in both power demand and steel production which slashed imports. China, which has generated relatively strong coal demand so far this year, has ratcheted up protectionist quotas on coal imports to support domestic coal producers. These have in turn throttled receipts of seaborne coal.

Covid-19 has exacerbated a trend of falling European coal imports over the past few years, accelerating the switch from coal-fired power to cheap natural gas. The losses in steel capacity and thus coking coal demand here will also take time to recover. We forecast global seaborne coal trade to contract by nearly 8% over 2020 as a whole, followed by a 2% recovery in 2021. Within this, there are some positive stories, such as growing demand in South East Asia, but these are not enough to offset the declines we see elsewhere.

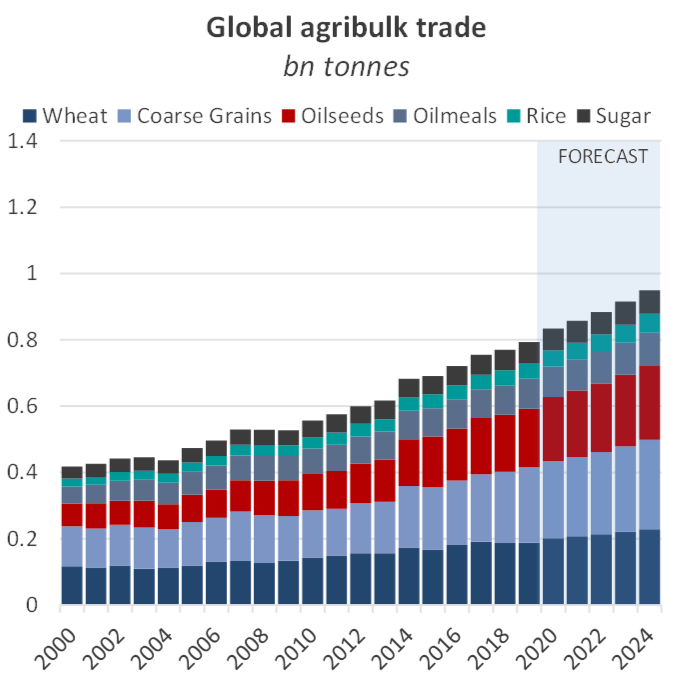

The Agribulks

In contrast to our outlook on coal, we remain positive on the grain trades and have upgraded our expectations for shipments. Taking the USDAs revised forecasts, the 2020/21 season is set to see grain trade grow by almost 4% versus the previous season. This marks an improvement of more than 2% on our previous forecasts.

Converting these to calendar-year estimates, we forecast soybean shipments from the major exporters to grow by 13% YoY over 2020 as a whole, with growth accelerating to almost 19% in 1H 2021. This is largely driven by continued growth in harvests in Brazil, Argentina and the US. Demand for this supply is underpinned by China’s enormous appetite, which seems to have fully recovered from the swine flu outbreaks a couple of years ago. Chinese imports from the US are set to improve over the coming months, following healthy sales activity between the two countries.

We also see wheat and coarse grain trade growth continuing over our forecast period, backed again by healthy volumes from the US and by greater production in the Black Sea.

Covid-19 has exacerbated a trend of falling European coal imports over the past few years, accelerating the switch from coal-fired power to cheap natural gas. The losses in steel capacity and thus coking coal demand here will also take time to recover. We forecast global seaborne coal trade to contract by nearly 8% over 2020 as a whole, followed by a 2% recovery in 2021. Within this, there are some positive stories, such as growing demand in South East Asia, but these are not enough to offset the declines we see elsewhere.

Supply side

In our modelling of future supply changes, the most significant revision is to scrapping. We had previously expected greater levels of Panamax and Supramax removals, but a combination of lockdowns at breaking yards earlier in the year and a relatively strong market over the past few months has limited the number of ships heading to the beaches. For the Panamaxes in particular, scrap-age units tend to find employment in Chinese coal cabotage trades, which have been lucrative over the past few months as import restrictions have forced coastal utilities to buy from local suppliers.

As such we have cut our forecast for removals this year, but we still expect this pool of scrap candidates to leave the fleet over the next year. In the longer term, we remain positive on the limited orderbook, which should keep supply growth in check. As we have covered over the past few weeks, this is a function of heightened uncertainty over emissions regulations, poor recent returns in the freight market and lack of access to financing.

We have however slightly increased our forecasts for future orders, as we expect some degree of price-driven speculative ordering. While we don’t see any solutions appearing imminently to comply with upcoming greenhouse gas reduction rules, we do expect newbuilding prices to soften, which will likely trigger ordering activity. In real terms, newbuilding prices are already at historically low levels, and further decreases will likely entice some interest in fleet renewal.

For more information on how these forecasts translate to shipping demand and utilization, please get in touch through your broker.