The World Steel Association (WSA) in its short-term outlook this month projects decent growth in global steel demand this year after a period of extreme market volatility emerging from several black swan events since the Covid outbreak. According to WSA projections, demand will increase by 1.7% this year to 1,793 mln mt and would grow further by 1.2% to 1,815 mln mt in 2025.

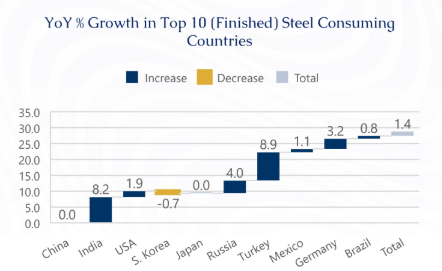

According to the latest WSA report, in absolute terms, India (144.3 mln mt, +8.2% y-o-y) has emerged as the strongest driver of steel demand growth, in contrast to a 1.7% growth globally. The report expects that India will keep up its strong performance, driven by the government’s impetus in structural construction spending during the election year. Additionally, higher infrastructure spending, growth in the property market, and the government’s emphasis on ‘Make in India’ (turning India into a manufacturing hub) will also fuel steel demand growth this year as well.

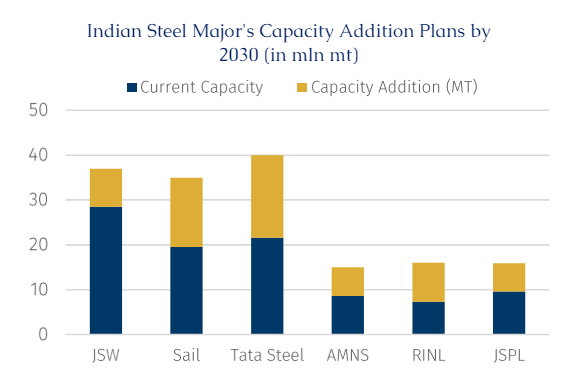

In 2018, India overtook Japan to become the world’s second largest steel producer. Since then, the steel production capacity of India has risen by 20%, or roughly 29 mln mt, to 171.35 mln mt as of February 2024. The real estate and infrastructure sectors have been the primary drivers. The government, in its annual budget, increased infrastructure spending by 11.1% YoY, to $134 million, for the fiscal year ending March 2025. Indian steel producers are preparing g themselves for a capacity increase in tandem with the rising domestic steel demand. According to the major steel producer’s annual capacity addition agendas published on their respective websites, about 10-12 mln mt of new Indian steelmaking capacity is expected to come online in the fiscal year ending March 2025. This will align production with rising demand. This is in line with the country’s target of raising per capita steel consumption from the current 87 kg to 158 kg and growing steel production capacity from the current 171 mln mt to 300 mln mt by 2030, thus meeting the robust growth and reducing import dependence.

Rising Input Costs:

Steel demand and raw-material costs have been impacted by several headwinds stemming from geopolitical uncertainties including Russia’s invasion of Ukraine, high inflation, low consumer spending, and the slowdown in economic activity. This has resulted in a structural shift in steel trade flows, thereby enabling India to emerge as an epicentre of growth in the sector. However, high raw-material price remains the major concern for the industry.

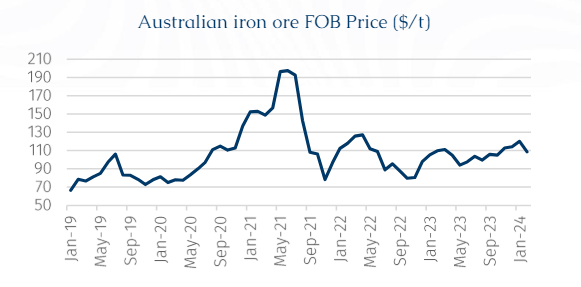

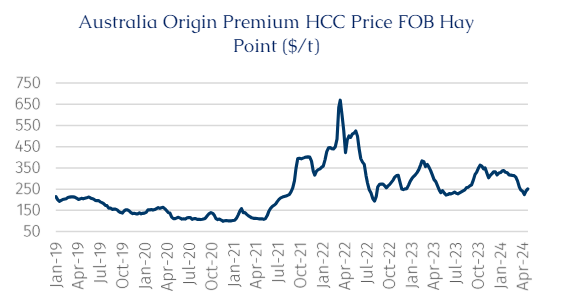

The cost of raw materials has increased sequentially even as steel prices have weakened. Prices for 62% Fe Australian iron ore increased dramatically from $80/mt FOB in 2019 before the pandemic to $110/mt in 1Q24. The cost of Australian premium hard coking coal has also increased from $190/mt FOB Hay Point in 2019 before the pandemic to $290/mt in 1Q24. Rising raw-material costs colliding with declining steel prices are weighing on steel mill profit margins.

The raw-material prices are not expected to cool because of the recent rebound in China’s economic recovery, which posted GDP growth of 5.3% in 1Q24. Steel demand in China is shifting from quantity to quality. In the last year, we have witnessed a fundamental change in China's steel consumption structure, with steady growth in steel consumption in minor industries (such as automotive, household appliances, and shipbuilding), partially offsetting the sluggish demand from the real estate sector. In general, steel demand in China appears to have entered an incremental decline phase, however, this may not be enough to create downwards price pressure.

(ref to BRS_Weekly Dry Bulk Newsletter_20240314_N107 for the details).

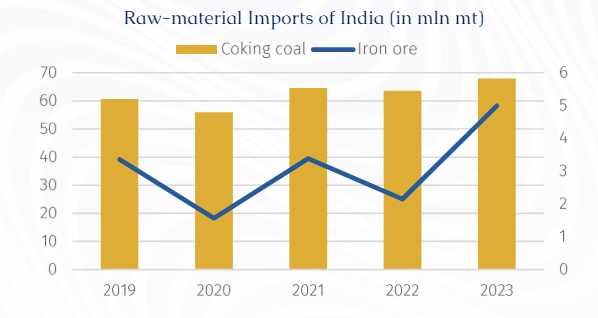

India’s growing demand for steel has raised the country’s consumption of iron ore and coking coal. The country is mostly self-reliant in iron ore due to its abundant availability; nonetheless, it imports about 3 mln mt of iron ore each year, mostly from Australia, Brazil and South Africa. The limited quantity of imports can be attributed to varying ore grades in multiple iron ore producing states, leading to price differences and higher inland logistics cost, making imports the most viable option for steel plants located on coastal areas. On the contrary, India remains 90% dependent on coking coal imports. Therefore, rising coking coal prices remain more of a concern than iron ore for Indian consumers.

According to AXSMarine data, India’s coking coal imports rose to a record 68 mln mt (+6.8% YoY) in 2023. Despite continuing to be the largest supplier, Australia’s overall proportion of shipments to India fell 20% in 2022 and 8% in 2023 YoY, with Russia and the US being the major beneficiaries offsetting the lost Australian volume, supporting Panamax demand. Although the lower cost of Russian coking coal has given Indian steel makers a margin advantage amid volatile steel demand and prices, buyers have shown resistance to buy more from Russia after the US Sanction while a few steel mills find difficulties in the usage of Russian coking coal for steel making. This may partially shift some volume to US in some cases, however, sourcing coking coal from US amid the Red Sea crisis and re-routing will make fuel costlier, pushing Indian buyers back to the traditional Australian market.

Exports:

The focus remains on the world’s largest steel producer – China as the steel industry closely monitors Chinese domestic demand. According to the AXSMarine data, Chinese steel exports increased by 30% to 56 mln mt in 2023, primarily due to weak domestic demand influenced by a sluggish property market. A significant increase in steel exports from China at a cheaper rate and narrow spreads has rendered steel exports from other origins less competitive. AXSMarine suggests that the majority of recent steel parcels out of China were destined for Asia followed by the UAE and Turkey.

Although India has maintained its role as the main supplier to the EU (65% or 2.8 mln mt), closely followed by Vietnam and the UAE, its long-term competitiveness may be curbed due to the cost of steel production. However, in the short run higher transportation cost resulting from the Red Sea crisis will limit shipments to the EU and the Middle East due to the combination of lower steel prices, higher input costs, higher levies, costly freights, and longer voyage duration. Typically, Indian steel mills increase their exports in response to a general increase in international steel prices. This is due to the fact that the cost of producing steel in the nation is approximately US$40/mt higher compared to other steel producing nations, according to the Indian steel major – JSW Steel.

Challenges Ahead:

According to the Indian Steel Ministry, India’s steel manufacturing capacity has already reached 161 million mt, comprising of three production methods: 67 mln mt by blast furnace-basic oxygen furnace (BF-BoF, typically associated with a higher CO2 intensity), 36 mln mt by electric arc furnace (EAF) and 58 mln mt by induction furnace (IF). The majority of the steel production in India is coming from the BF route and the current fleet of BFs in India is relatively young indicating the pressing need for energy efficiency measures.

The steel sector faces significant challenges related to carbon emissions amidst the comparatively slower demand in the global market. Furthermore, the EU's Carbon Border Adjustment Mechanism (CBAM) poses a significant challenge to the Indian steel industry as it accounts for 12% of India’s greenhouse gas emissions with an emission intensity of 2.55 tonnes CO2 per tonne of crude steel due to the predominance of coal in steel production combined with low raw material quality. This compares to a global average of 1.9 tonnes CO2 per tonne of crude steel. With the introduction of the EU's CBAM, Indian steel producers and exporters are already working towards minimising emissions through switching to DRI-based production, increasing the use of scrap steel, and/or transitioning to renewable energy sources, particularly solar by March 2031.

Conclusion

Evidence suggests that the Indian steel industry is backed by a plethora of schemes and incentives announced by the Central government. India produced 126.26 mln mt of crude steel and 122.28 mln mt of finished steel in 2023 and remained a net exporter as it shipped 6.72 mln mt of finished steel against the 6.02 mln mt of imports. Growing steel production translates into growing coking coal demand, which would support more tonnage demand for gearless bulkers in the Pacific while rising finished steel exports will support more geared bulkers transiting to Atlantic, and consequently better freights.