The sentiment of freight rates persists weaker with the number of ballasters increasing, while the number of vessels in port congestion around China is increasing in the last days of April. It seems that the number of vessels in congestion at Chinese ports will continue to hold firm levels as the zero-COVID policy has created severe bottlenecks at major port hubs, like Shanghai, Tianjin, and Ningbo.

The latest situation with Chinese policy measures has led to a decreasing evolution in the demand and lower commodity prices. In the iron ore market, Prices for iron ore cargoes with a 63.5% iron content for delivery into Tianjin tumbled to around $135/t, a level not seen in over a month. In the meantime, weak demand from the construction sector has already led to a pile-up in steel inventory during what should be one of the year’s main periods of activity.

In the coal segment, the ongoing geopolitical situation has escalated prices. Newcastle coal futures, the benchmark for the top consuming region of Asia, fetched $326/t, close to a five-week high of $331 reached last Thursday, due to skyrocketing demand amid tight supplies of alternative energy products and sanctions on Russian coal. Top consumers are still seeking to find alternative supplies to replace Russian supplies, buying from more distant countries such as Australia and South Africa.

In the grain market, prices also posted firmer. Chicago wheat futures rose above $10.8 per bushel, rebounding from the two-week low of $10.6 recorded on April 25th as unfavorable winter crop conditions from North America spurred further supply concerns. Wheat prices remain 28% higher than before the Russian invasion of Ukraine, amid interrupted exports from the Black Sea.

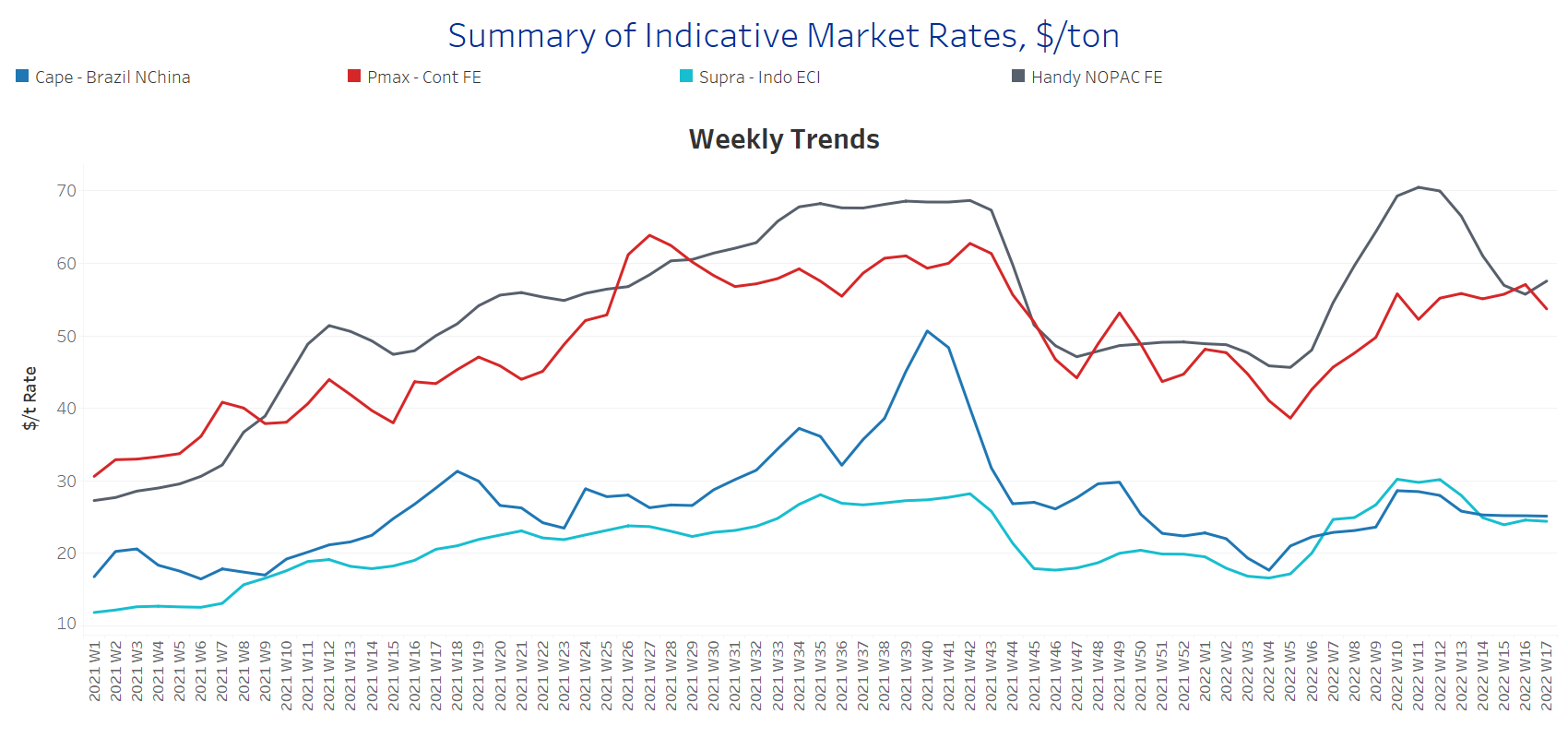

SECTION 1 - FREIGHT - Market Rates ($/t) - Weaker

‘The Big Picture’ - Capesize and Panamax Bulkers and Smaller Ship Sizes

The freight sentiment switched to negative for the last days of April, however, there are signs of revival in the Handysize segment following four weeks of successive declines.

Capesize Brazil-to-North China freight rates dropped to $22/t, almost $3.5/t less than the previous week, and only four dollars above the lows of Week 10 of this year ($18/t).

Panamax Continent-to-Far East freight recorded a sharp decrease to $50/t, down $6/t from the previous week, but still robust compared to the low at the end of Week 4 ($39/t).

Supramax Indo-to-ECI freight rates dropped further below $24/t, while the last high remains the Week 12 ~ $30/t.

Handysize NOPAC-to-Far East freight rates posted signs of increase towards $56/t, but still weaker than the peak of Week 11 - ($71/t).

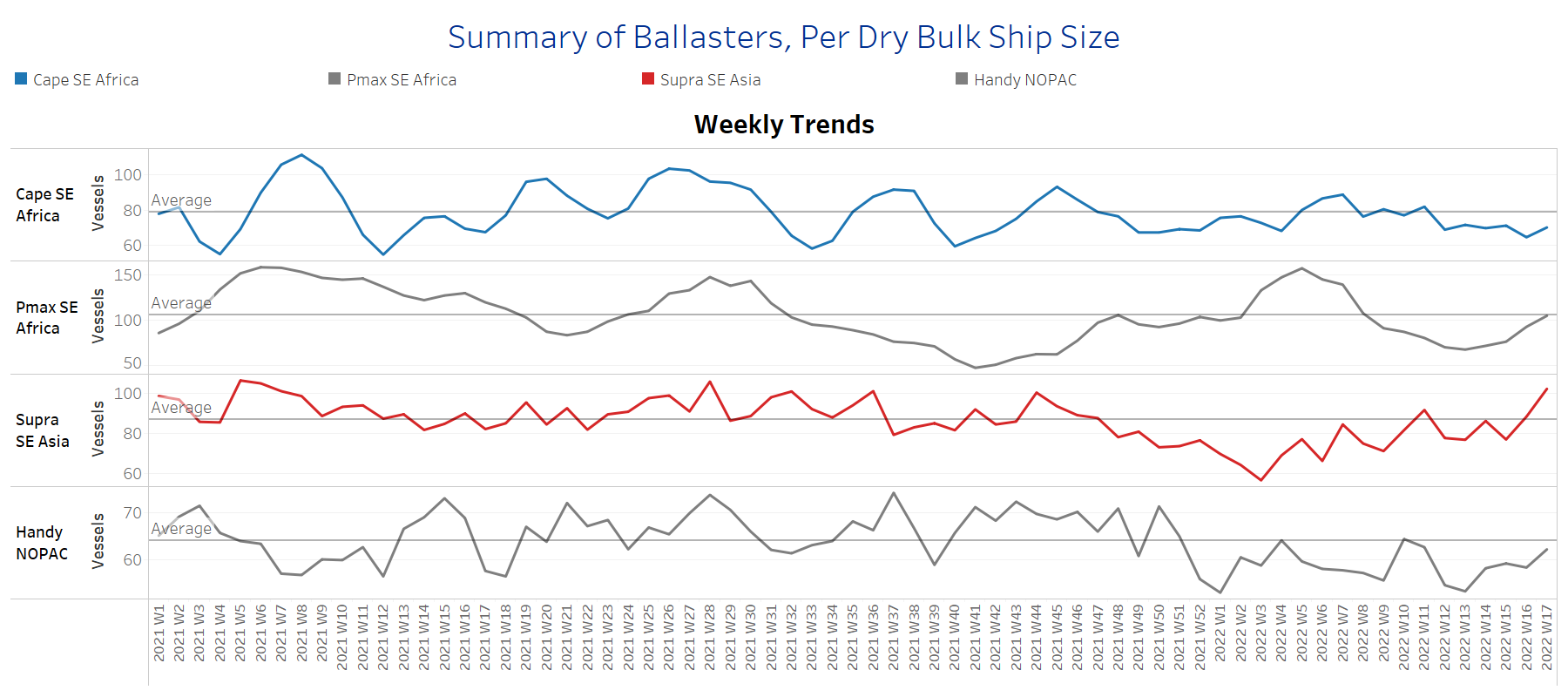

SECTION 2 - SUPPLY - Ballasters View

Number of Vessels - Increasing

Supply Trend Lines for Key Load Areas

The number of ballasters signals an increasing trend for all vessel size categories for the second consecutive week. Despite the sharp increase in the Supramax segment, both the Supramax and Handysize segments remain below the one-year average.

Capesize SE Africa: The number of vessels sailing in ballast increased to around 69 vessels, 5 vessels more than the previous week. It is interesting to note that the evolution of ballasters is around 10 vessels less than the one-year average, and the last peak was during week 11 with around 82 vessels.

Panamax SE Africa: The number of vessels sailing in ballast increased to the one-year average of 106 vessels, 37% up from the low of Week 15.

Supramax SE Asia: The number of vessels sailing in ballast increased to 105 vessels, posting the same increase with the Panamax segment compared to the levels of Week 15.

Handysize NOPAC: The number of vessels sailing in ballast held a steady momentum with around 60 vessels for the last three weeks, 4 vessels less than the one-year average.

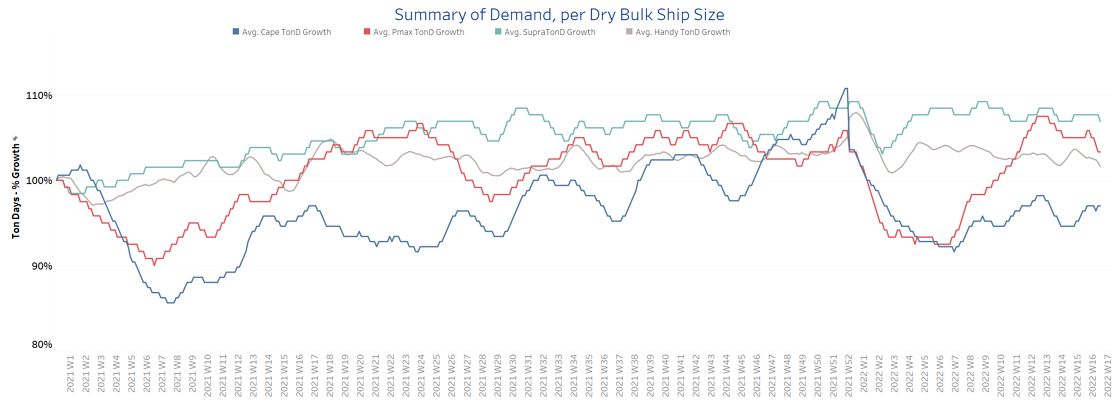

SECTION 3 - DEMAND - In Ton Days

Decreasing

The overall trend of demand ton-days continues decreasing, with the Handysize and Panamax segments showing a clear downward direction, while signs of revival are seen in the Capesize segment since last week.

Capesize demand ton-days: There is a sustained upward trend compared to the low of Week 14.

Panamax demand ton-days: We see signs of a strong downward revision for the last days of April, although it seemed a steadiness the last week.

Supramax demand ton-days: There is flat momentum for three consecutive weeks with insignificant spikes or lows.

Handysize demand ton-days: There are no signs of a shift from the slow growth following the last peak during Week 15.

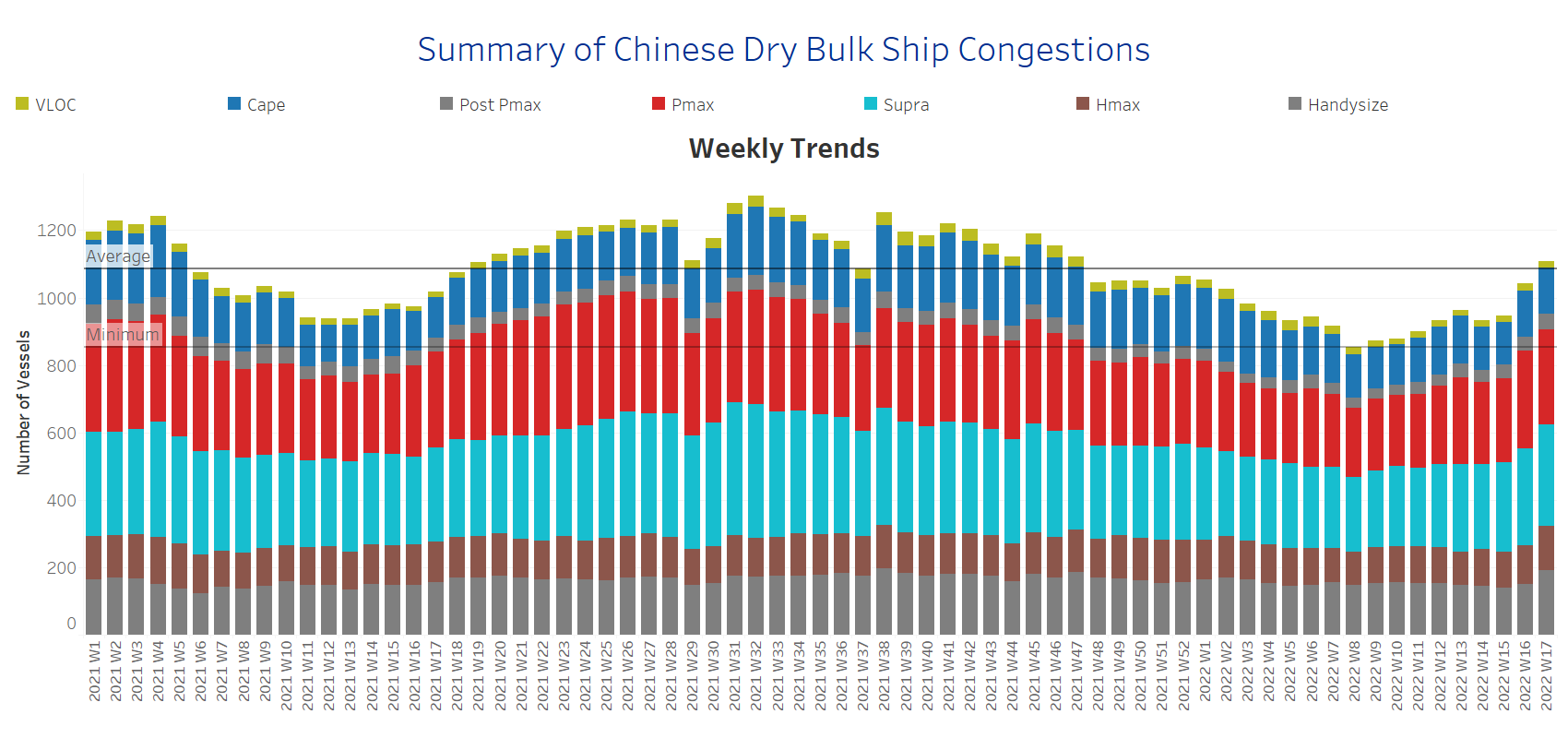

SECTION 4 - CHINESE PORT CONGESTIONS -

Number of Vessels - Increasing

Dry bulk ships congested at Chinese ports

Dry bulk ships in congestion recorded a further sharp increase following last week’s spike, stemming mainly from the Handysize segment, while the situation in the Panamax segment seems to have eased.

Capesize: The number of ships in congestion held almost the same levels as the previous week at around 138, only 2 vessels less than the previous week.

Panamax: The number of ships remains at increased levels of previous days at 286, 4 vessels less than the previous week.

Supramax: The number of ships in congestion surpassed 300, a 20% increase since the ending of Week 14.

Handysize: The number of ships in congestion fetched 196, a 40% increase since the ending of Week 15.

Data Source: Signal Ocean Platform