By Mark Nugent

With the Capesizes less exposed to the impact of the Ukraine—Russia conflict, we look at what is currently driving the Capes higher and what risks may be present.

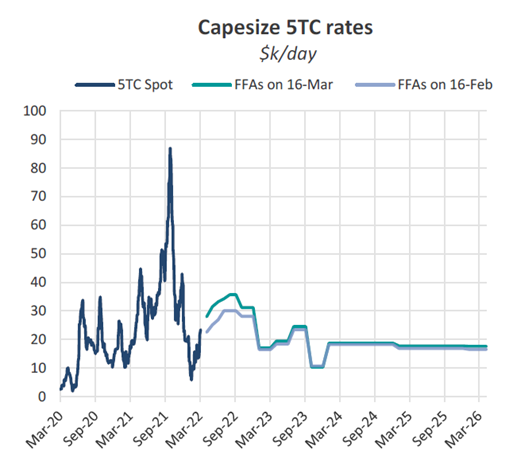

Following a 15.4% decline on the day following the onset of the war in Ukraine, Capesize 5TC spot rates have increased by 54.0% to $21,596 per day. Less affected by shipments in the Black Sea compared to the smaller size vessels, the region accounted for just 2.5% of Capesize demand in 2021. One factor driving the upturn has been the sharp rise in crude oil prices, in which VLSFO reached all-time highs above $1,000 per tonne. Sentiment has grown in the Cape market as more longer-haul coal cargoes to Europe are reported and iron ore volumes out of Brazil have started to improve. However, there may be other factors influencing the rebound in the Capesize 5TC average, which hit its low in 2022 on January 26 at $5,826.

The C16 backhaul Capesize rate, although lower in the past couple of days, has risen by $11,750 per day following the war in Ukraine as vessels leaving China are increasingly bid higher to do coal stems for European buyers from locations other than Russia. As buyers scramble for energy supplies it is more efficient to buy coal in larger quantities, particularly with fuel oil at such high prices and the Capesizes trading at a $4,053 per day discount to the Panamaxes based on current timecharter averages.

Coal shift begins

Capesize coal trade has remained strong so far in 2022, with 61.2m tonnes loaded across January—February, increasing by 11.3% YoY. However, a decline in demand from China as domestic production is ramped up has slowed overall Cape employment from coal, declining by 9.2% YoY in February. Last month, 1.2m tonnes of coal arrived into Chinese ports on Capesizes, declining by 64.5% YoY and the lowest level since November 2020.

Although the EU has not officially sanctioned imports of Russian coal, self-sanctioning by many European buyers has resulted in some volumes starting to load from further afield. In February, Colombian coal loadings on Capesizes to Europe more than doubled YoY to 1.4m tonnes and the highest since December 2019. So far in March, 686k tonnes has loaded on Capes in Colombia for European destinations. This is already higher than total loadings for this trade in March of the previous two years. The Colombian government last week announced it was discussing an increase in coal exports with the country’s largest producers due to increased demand from European and Central American end-users, implying this trend is likely to continue. From Indonesia, so far 507k tonnes of coal has loaded on Capes destined for Europe in March, the highest level since January 2019. With Chinese demand tapering so far in 2022, there is likely to be more Indonesian volumes available to other buyers, such as Europe, going forward. From other sources, such as Canada and South Africa, we have so far not seen a significant increase in Capesize coal trade to Europe.

Iron ore trades mixed

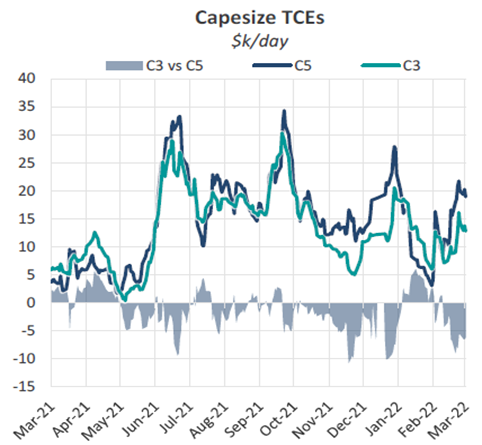

Out of Australia, iron ore volumes have been relatively strong so far in 2022. Across January-February of this year, 139.0m tonnes of iron ore loaded on Capes, increasing by 3.4% YoY. As Australian volumes have remained steady, many vessels have opted to stay in the Pacific and continue doing C5 voyages rather than ballast past Singapore in search of a Brazilian cargo. The current premium to do a C5 voyage versus C3 is $6,161 per day. Delays in Chinese ports will likely cause exporters in Australia to look for prompt vessels, keeping rates in the Pacific healthy. Tonnage supply in Brazil has moderately increased in recent weeks, as slightly higher volumes convince more ballasters to head West and vessels in India/PG which typically do Black Sea trades make the trip across the south Atlantic.

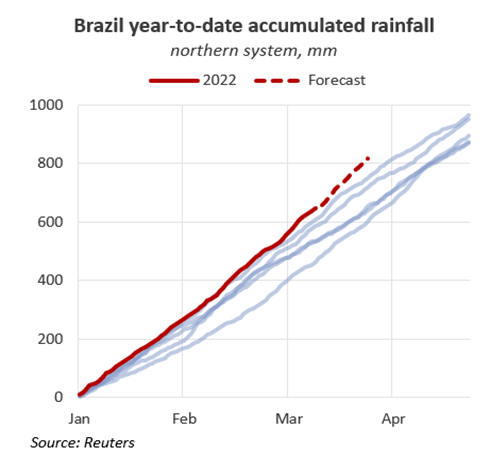

In Brazil, the seasonal rainy season has been more harsh than in previous years, particularly in the northern system where the large mining region of Pará is located. Year-to-date accumulated precipitation in northern regions is 10.8% higher YoY and higher than levels at this time of year in each of the past 5 years. Shipments from Brazil across the first two months of the year decreased by 6.0% YoY to 44.9m tonnes as mine and port operations were affected. Although conditions moderately improved in recent weeks, current forecasts indicate more rain may be on the way and could delay a substantial improvement in iron ore volumes out of the region.

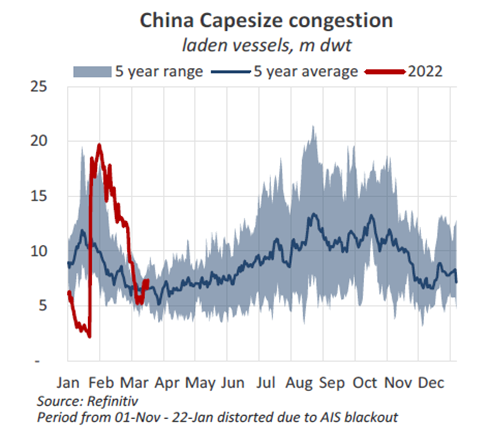

Fresh lockdowns in China

In the last week, a surge in Covid-19 cases in China has triggered a wave of lockdowns in several regions across the country that may disrupt port operations in the coming weeks. Although we have seen the seasonal unwind in Capesize congestion in China following the Lunar New Year, in the last week we have seen a slight uptick again, with this likely to compound in the coming days. Queues of laden Capesizes have grown by 26.0% WoW to 7.4m dwt and currently lie 12.3% above the 5-year average for this time of year.

The scope for a rebound in congestion, as a result of the lockdowns, is now higher given the constraints ports are under when employee infections rise. This is naturally reliant on any lockdowns being prolonged past the one week in which they are currently in place. With China’s Zero-Covid policy still in place and cases rising, it would not be surprising to see these extended. Capesize vessels have also began to slowdown en route to Chinese ports, potentially in anticipation Covid-19 measures are eased and queues are cleared by the time they arrive. Average voyage speeds of Capes discharging in China have declined by 0.15 to 10.47 knots so far in March compared to those in February. In comparison, all laden Capesize voyages are travelling, on average, 0.18 knots faster at present. This slowdown in speeds, particularly towards China, should help support the market going forward as this trend continues.

However, the downside to Chinese lockdowns, in the case these are prolonged and more are installed if cases continue to rise, is reduced economic activity. Some factories in the manufacturing hub of Shenzhen have reportedly halted operations altogether while lockdown is in place. While this region has a greater focus on consumer goods, further lockdowns could be extended to raw-material intensive industrial regions if the Covid-19 situation worsens.