by Maria Bertzeletou

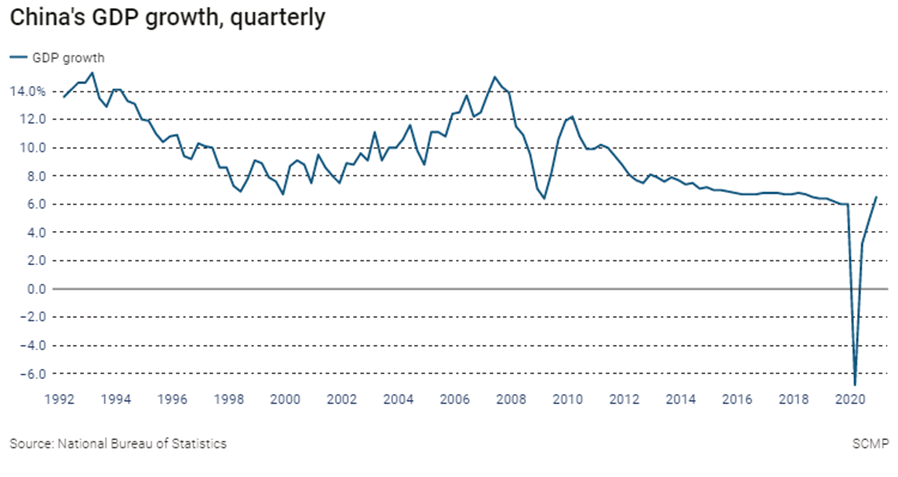

China’s economy grew at the slowest pace in more than four decades last year despite a rebound after the country’s coronavirus outbreak. The 2.3% expansion is the lowest figure since the Chinese economy embarked on major reforms in the 1970s. The National Bureau of Statistics (NBS) said 2020 was a “grave and complex environment both at home and abroad” with the pandemic having a “huge impact.”

The figure was a marked slowdown from 2019 growth of 6.1% – itself already the lowest in decades – with the country hit by weak domestic demand and trade tensions.

During the first quarter of this year Chinese GDP grew at a faster-than-expected rate of 6.4 percent compared to the same period last year and ahead of the 6.3 per cent expected according to a Reuters poll. The figure matched the 6.4 per cent growth posted in the final quarter of 2018, but was significantly below last year’s first-quarter growth figure of 6.8 per cent.

Premier Li Keqiang warned that there are new uncertainties ahead for economy. Beijing is keen to maintain a cautious view towards the prospect for the world’s second largest economy, highlighted by setting a modest economic growth target of “above 6 per cent” for 2021, and is looking to keep necessary fiscal and monetary support in place. He said that the country will continue to impose targeted structural tax cuts in a bid to keep the intensity of ensuring jobs, livelihoods and market entities, while US President Joe Biden is looking to raise corporate income tax rates to fund his proposed US$2.3 trillion infrastructure spending plan.

U.S. GDP shrank by 3.5% in 2020 as the country’s uncontrolled COVID-19 outbreak shattered the economy. China, meanwhile, largely contained the virus and became the only major economy to report economic growth last year. But now, the U.S. is pairing its $1.9 trillion stimulus plan with a successful vaccine rollout nationwide, which, is causing China to become very nervous about America’s economic rebound. The $1.9 trillion stimulus package could see the U.S. economy outpace China’s for the first time in 45 years. According to World Bank data, the U.S. last surpassed China’s growth rate in 1976, with annual GDP growth of 5.4% compared with China’s –1.6%.

Whether it’s 6% or 8% GDP growth, we do know that China is going to overwhelmingly be the best growth story in the global economy. Next year, the U.S. presumably will start to bounce back. In 2021—this is unlikely but possible—the U.S. could grow more than China.

Economists have different figures for when they think China in real terms—the Chinese GDP—will overtake the United States. 2028 maybe the year for China that will overtake the United States.

The U.S.’s $1.9 trillion package actually prolongs the time in which China will actually surpass the U.S. Because that stimulus package is not a one-year package, it is a 10-year package. That’s going to bring growth to the U.S. for quite some time. It will also depend on how much China needs to crack down on its financial risk. The Chinese government has a lot of tools to manage the market, particularly this year, which is the 100th anniversary of the Communist Party.

The challenge for the dry bulk shipping demand is that although China has a GDP growth target for 2021 of "above 6%, ", this is below the market consensus of 7%-9%, indicating that stable economic growth, deleveraging and decarbonizing of the economy will be priorities for the year. The Chinese government is aiming at quality of growth and not simply maintaining high GDP growth, which is set to adversely impact infrastructure and property steel demand, as well as steel production.

The main challenge over the next five years for the growth of seaborne dry bulk ton miles is ChIna’s target to strengthen management and control of its strategic mineral resources, as it set out a five-year development plan, without providing any details on how it plans to secure key supplies and boost self-sufficiency.

New five-year plan for 2021-25

Steel / iron ore: The country pledged to improve its reserve security capabilities and conduct a new round of ore prospecting in the next five years, according to the plan, which serves as a blueprint for economic and social development between 2021 and 2025. The industry ministry said in December that China aims to build one or two globally significant overseas iron-ore mines by 2025 to boost supply and enhance its pricing power.

For the steel sector, China vowed to promote green transformation. China aims to complete ultra-low emission upgrade for 530-million tonnes of steel capacity and clean production upgrade for 850-million tons of cement and for 460-million tons of coke capacity, according to the plan.

Around 620-million tons of crude steel capacity had already been upgraded to ultra-low emissions or were in the process of being upgraded by the end of 2020. For 2021, China said it will continue to push forward supply-side reform and mergers and acquisitions in the steel sector, according to the state planner report also released on Friday during the annual parliament meeting. China's Iron and Steel Association expected steel demand to grow slightly in 2021.

Coal power: China will be investing far more in coal power over the next five years that only modestly increased renewable ambitions. Environmentalists had been hoping China’s five-year NDP would provide a roadmap towards carbon neutrality by 2060. However, the plan signals little urgency in cutting greenhouse gas emissions and revealingly also lacks a cap on total energy consumption. China plans to reduce carbon emissions per unit of GDP by 18%, being the same target as the previous five years. With overall economic growth likely around 6% in 2021, this allows for a net increase in carbon emissions.

In April, news came to light for a huge stake in iron ore mine in Guinea that may cut China’s dependence on Australia. The Simandou mountains, a 110km (68-mile) range deep in the interior of southeastern Guinea, is home to the world's biggest untapped supply of high-grade iron ore, and China believes it could help cut its reliance on Australian imports amid trade tensions. The huge project, which holds an estimated 2.4 billion tonnes of iron ore graded at over 65.5 per cent, could diversify China's supply chain but may not cut out Canberra completely, analysts say. Australia is the source of about 60 per cent of China's iron ore imports.

The current dry bulk fundamentals appear alluring for the current year as market expectations indicate demand growth for dry bulk shipping to total almost 3x the growth in net new supply, and although utilization is still well below the record high levels of the 2000s, directionally, utilization is heading to new multi-year highs that have the potential to push shipping rates much higher.

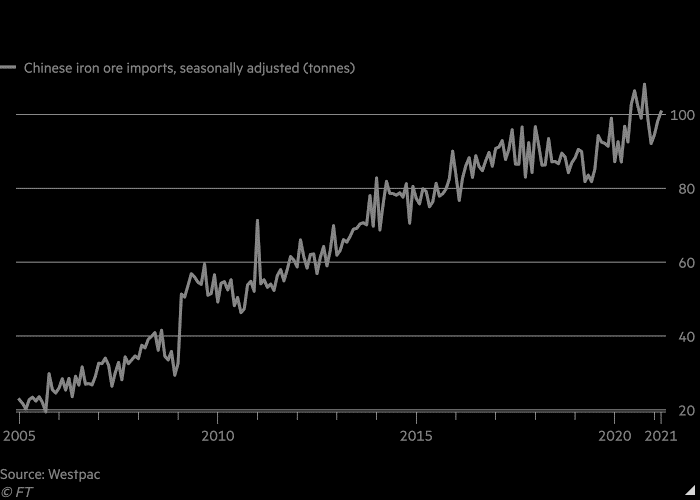

During March, imports of iron ore in China have jumped a whopping 19% to 102.11 million tonnes in March vs the prior year according to Tuesday’s official customs data. A Reuters report highlighted that world’s top base metal and iron ore consumer brought in 283.44 million tonnes of the steelmaking ingredient in the first quarter, up 8% on an annual basis, data from the General Administration of Customs showed. China’s iron ore imports from Australia surged in March while some analysts have warned China’s demand for Australian ore has peaked as alternative supplier Brazil comes back on line and the country develops new sources in Africa, the latest trade data was good news for Australian miners amid buoyant iron ore prices.

However, in the longer term, the Chinese steel industry is very emissions heavy, and with China’s commitments to peak carbon emissions by 2030, and reach carbon neutrality by 2060, the steel-making industry will not be able to escape changes combined with the plans of Chinese government to increase its self-sufficiency on strategic mineral resources.

How Chinese steel demand affects Australia

In a sign of falling appetite in terms of volume alone, shipments of iron ore from Australia to China have dropped every month since September. In February, imports stood at 51.5m tonnes, compared with 70.6m in July, according to Census and Economic Information Center data. As the chart below shows, broader Chinese demand for iron ore has eased off its recent highs, though the fall has been less dramatic than that experienced by Australia.

But the value of iron ore shipments from Australia in February hit $7.8bn, its highest level for any month on record, CEIC data shows, due to a surge in the price of commodities. Australia also faces competition, particularly from Brazil, where shipments are up 19 per cent in 2021 so far, according to UBS, in contrast to struggles last year.

S&P Global Platts expects steel demand from the construction sector to remain high in 2021, even in the face of government pressure. But in a recent note, it said that urbanisation, which had been the “core driver of China’s property development and steel consumption over the past 20 years”, typically became less steel-intensive after the urbanisation rate breached 60 per cent. It noted that urbanisation in China exceeded 60 per cent in 2019 and was expected to reach 70 per cent by 2030.